Key Concepts and Terminology Explained

The legal field relies heavily on specific terminology that can easily confuse anyone outside the profession. To make informed decisions about your financial and legal future, you first need to understand the language used in these documents. Let us demystify the core concepts surrounding legal authority aging and surrogate decision-making.

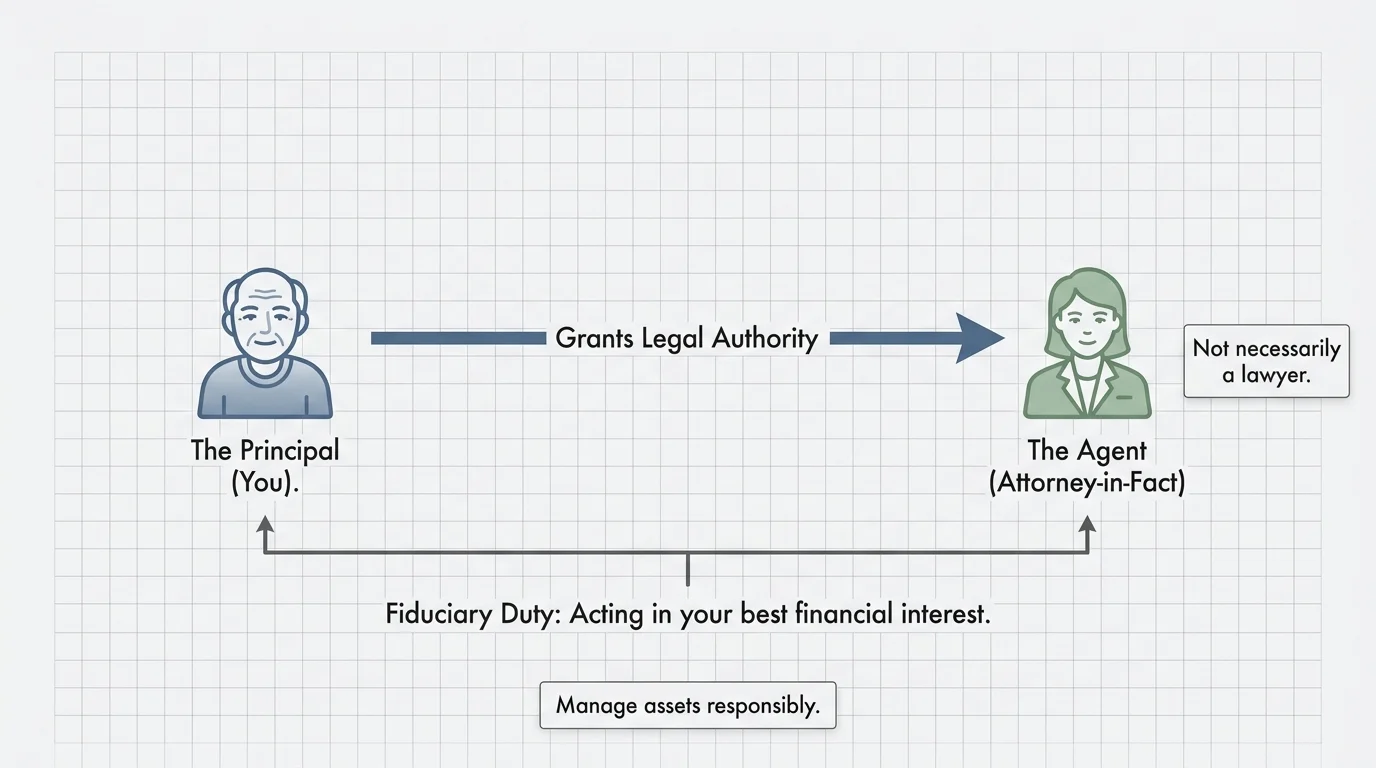

The Principal and the Agent

Every Power of Attorney involves two primary roles. You are the Principal—the person who creates the document and grants authority. The person you select to act on your behalf is the Agent, sometimes referred to as your “attorney-in-fact.” Despite the title, your agent does not need to be a lawyer. Your agent is simply the trusted individual—a spouse, an adult child, a sibling, or a close friend—whom you authorize to manage your affairs. The agent carries a fiduciary duty, meaning the law requires them to act strictly in your best financial interest, manage your assets responsibly, and avoid any conflicts of interest.

Durable vs. Non-Durable Authority

The concept of “durability” is arguably the most critical element for seniors to understand. A standard, non-durable document automatically becomes invalid the moment the principal becomes mentally incapacitated. Obviously, if your goal is to ensure someone can manage your finances during a severe illness or cognitive decline, a non-durable document fails exactly when you need it most.

A Durable Power of Attorney contains specific legal language stating that the agent’s authority remains fully intact even if you lose your mental capacity. This durability ensures continuous financial management. Your agent can keep paying your property taxes, managing your investment portfolios, and interacting with your creditors without missing a beat, effectively preserving your financial stability during a health crisis.

Financial vs. Medical Authority

While people often talk about these documents as a single entity, you generally need separate documents for different areas of your life.

- Financial Power of Attorney: This document exclusively covers matters related to your money, property, and business affairs. It allows your agent to deposit Social Security checks, manage real estate, negotiate with debt collectors, and handle tax obligations.

- Medical Power of Attorney (Advance Directive or Healthcare Proxy): This document authorizes someone to make healthcare decisions for you—such as consenting to surgery, choosing a rehabilitation facility, or making end-of-life care decisions—when you cannot communicate with doctors yourself.

Because the skills required to manage a complex investment portfolio differ significantly from the emotional fortitude needed to make life-and-death medical choices, you can choose different agents for each role. For example, you might designate your financially savvy daughter as your financial agent and your empathetic, medically knowledgeable son as your healthcare agent.

General vs. Limited Authority

You possess complete control over the scope of power you hand over. A General Power of Attorney grants comprehensive authority, allowing your agent to perform virtually any financial transaction you could execute yourself. This sweeping authority is typical in comprehensive estate planning.

Conversely, a Limited (or Special) Power of Attorney restricts the agent to specific tasks or a particular timeframe. For instance, if you plan to travel overseas for six months, you might grant a limited authority allowing your agent only to sign closing documents on a specific real estate transaction while you are away. Once the task is complete, the authority terminates.

Springing Authority

A Springing Power of Attorney remains dormant and only “springs” into effect upon the occurrence of a specific event—usually your verified medical incapacity. While this appeals to individuals hesitant to grant immediate control over their finances, it can create significant practical hurdles. To activate a springing document, your family typically needs formal written declarations from one or two physicians certifying your incapacity. This requirement can delay urgent financial actions, leading to late fees, missed investment opportunities, or temporary lapses in vital insurance coverage while your family navigates the medical bureaucracy.