A Practical Guide to 7 Estate Planning Steps Adult Children Should Take Before A Parent Turns 80

Taking action before a parent turns eighty provides a critical window of opportunity. At this stage of life, most seniors still possess the mental capacity required to sign legal documents, but the statistical likelihood of facing cognitive decline or sudden physical illness is accelerating. Use the following seven practical steps to navigate this transition smoothly and effectively.

Step 1: Initiate the Conversation Openly and Empathetically

The most significant barrier to effective preparation is the profound reluctance to discuss aging, decline, and death. Many adult children fear that bringing up these topics will make them appear greedy or morbid. To overcome this hurdle, you must frame the conversation around their protection, their legacy, and your desire to carry out their exact wishes. Choose a calm, quiet time to talk—not during a holiday gathering or immediately following a medical scare.

You might open the dialogue by mentioning a friend who recently navigated a difficult probate process or by discussing your own financial preparations. Emphasize that your primary goal is to ensure they receive the exact medical care they prefer and that their hard-earned assets are protected from unnecessary taxation and legal fees. By positioning yourself as their advocate and partner, you foster a cooperative environment rather than a defensive one.

Step 2: Locate and Organize Important Documents

An immaculate legal document provides zero value if no one can find it during a crisis. You and your parents need to conduct a comprehensive inventory of all vital records and store them in a secure, accessible location. This inventory should include birth certificates, marriage licenses, divorce decrees, military service records, and Social Security cards. Furthermore, you must track down the original copies of any existing wills, trusts, and advance directives.

Create a detailed master list of family finances. Document all checking and savings accounts, investment portfolios, retirement funds, pensions, and life insurance policies. Include the names of the financial institutions, account numbers, and the contact information for any financial advisors or brokers they currently use. Do not overlook digital assets; compile a secure list of usernames, passwords, and security questions for email accounts, online banking portals, and social media profiles. Consider utilizing a secure password manager or a fireproof home safe, ensuring that you and at least one other trusted family member know the combination or master password.

Step 3: Establish a Durable Power of Attorney

A durable power of attorney for finances ranks among the most vital legal instruments an older adult can execute. This document authorizes a trusted individual—often an adult child—to manage financial affairs, pay bills, file taxes, and oversee investments if the parent becomes physically or mentally incapable of doing so. The term durable means that the document remains valid even after the principal loses cognitive capacity.

Without this document in place, you cannot legally access your parent’s bank accounts, cancel their subscriptions, or sell their property to fund their medical care. Instead, you would be forced to petition a court for an adult conservatorship or guardianship. That court process is notoriously expensive, incredibly time-consuming, and emotionally draining. Establishing a durable power of attorney while your parent is healthy eliminates this tremendous burden.

Step 4: Set Up Advance Healthcare Directives

Medical emergencies leave no time for family debates. Advance healthcare directives provide explicit, legally binding instructions regarding your parent’s medical preferences. This category typically includes two distinct documents: a living will and a healthcare power of attorney.

A living will outlines the specific types of medical treatments your parent wants or refuses to receive at the end of life. It covers critical decisions regarding artificial nutrition, hydration, mechanical ventilation, and cardiopulmonary resuscitation. A healthcare power of attorney designates a specific person, called a healthcare proxy or surrogate, to make medical decisions on their behalf if they cannot communicate with doctors. Having these documents executed ensures that medical professionals respect your parent’s values and spares your family the agonizing burden of making life-or-death decisions blindly.

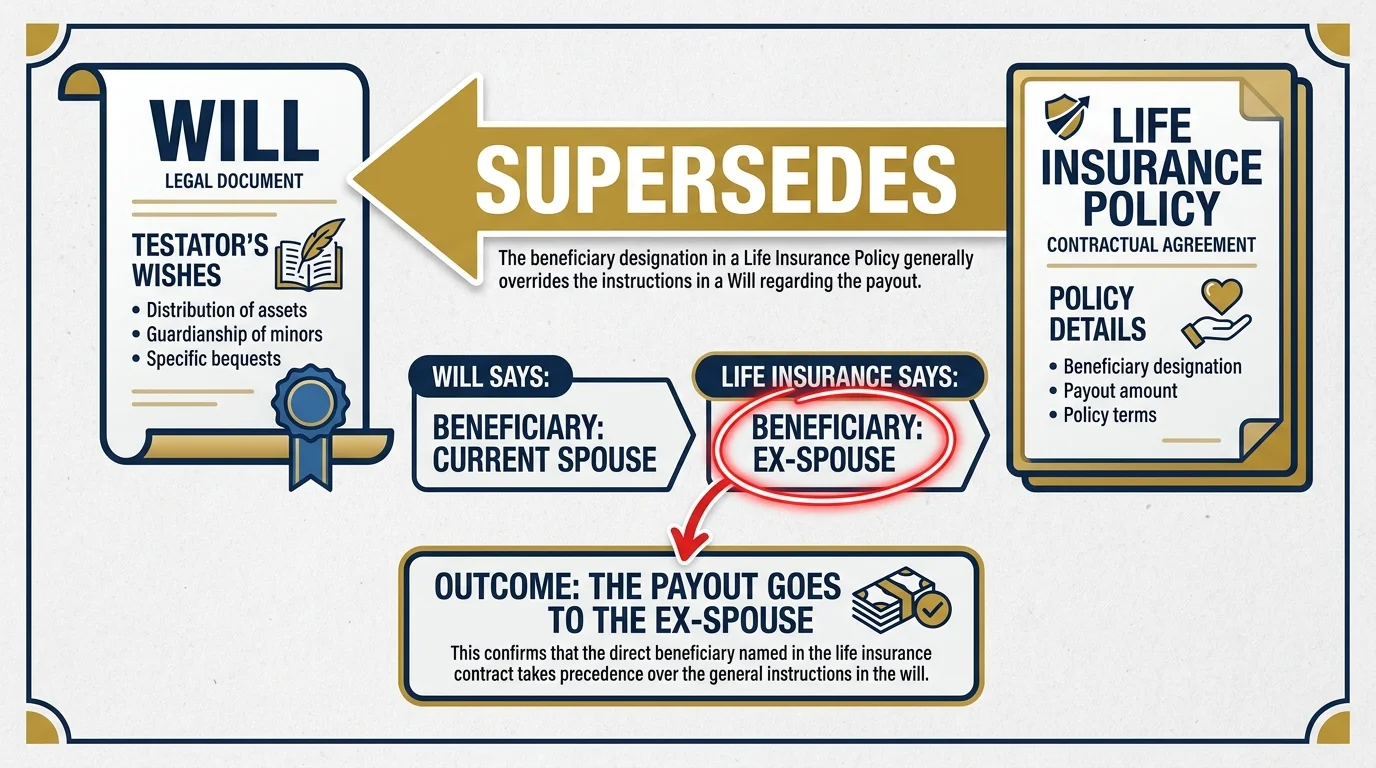

Step 5: Review and Update Beneficiary Designations

Because beneficiary designations on financial accounts bypass the probate process and override instructions in a will, they require meticulous attention. Over the decades, people often forget who they listed on their 401(k)s, IRAs, and life insurance policies. Major life events—such as divorces, marriages, the birth of grandchildren, or the passing of a designated beneficiary—necessitate immediate updates to these forms.

Sit down with your parents and request the current beneficiary designation forms from every financial institution they use. Ensure that they have listed both primary and contingent beneficiaries. A contingent beneficiary serves as a backup, receiving the assets if the primary beneficiary passes away before your parent. Correcting these forms takes only a few minutes but prevents devastating legal mistakes that can redirect an entire inheritance to the wrong person.

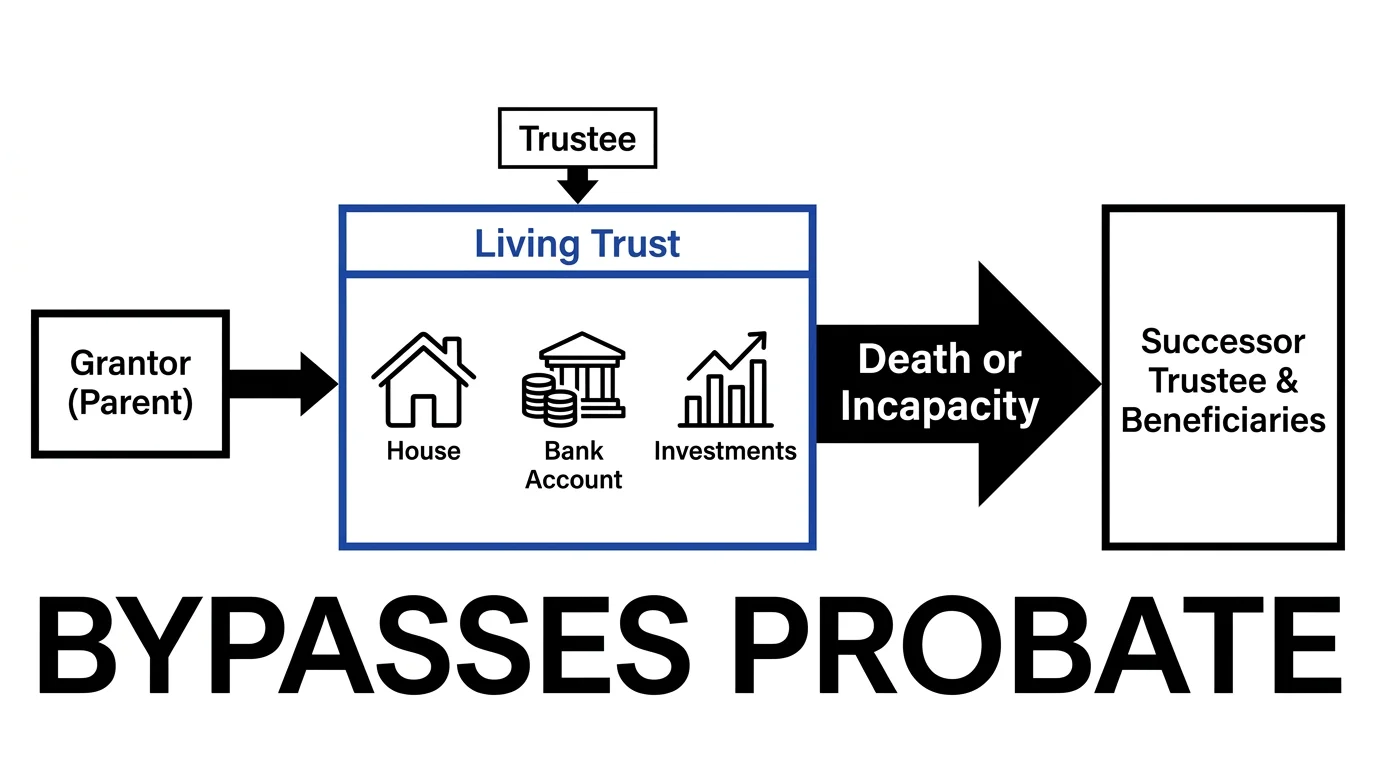

Step 6: Assess the Need for a Living Trust

While a standard last will and testament serves as the foundation of basic planning, many families discover that a revocable living trust offers superior benefits. If your parents own real estate in multiple states, possess significant assets, or highly value family privacy, a trust is likely the better vehicle for their legacy.

When assets are formally transferred into a living trust, the successor trustee can distribute them to the heirs almost immediately after the parent’s death, completely bypassing the public and sluggish probate court system. Furthermore, trusts offer unparalleled control over how an inheritance is distributed. For example, if a parent wishes to leave money to a grandchild but wants to ensure the funds are used strictly for college tuition rather than frivolous spending, a trust can stipulate those exact terms. Evaluate your parent’s specific financial landscape to determine if the upfront cost of establishing a trust outweighs the eventual costs and delays of probate.

Step 7: Map Out Long-Term Care and Financial Strategies

The cost of assisted living facilities, memory care units, and in-home nursing care can rapidly deplete a lifetime of savings. Before a parent reaches eighty, you must actively evaluate how the family will fund these potential expenses. Review any existing long-term care insurance policies to understand the daily benefit limits, elimination periods, and specific coverage triggers.

If long-term care insurance is unavailable or prohibitively expensive, you need to assess their eligibility for government assistance programs like Medicaid. Medicaid planning requires immense foresight because the government utilizes a five-year look-back period. If your parents give away money or transfer property to you within five years of applying for Medicaid, they will incur severe penalty periods during which the government refuses to pay for their care. Structuring their assets properly well in advance ensures they receive the care they deserve without impoverishing a healthy surviving spouse.