Common Mistakes and How to Avoid Them

Navigating the intersection of family dynamics and the legal system is inherently fraught with potential pitfalls. Even families with the best intentions frequently make critical errors that jeopardize the financial stability and emotional harmony of the surviving relatives. Understanding these common legal mistakes is the first step toward preventing them.

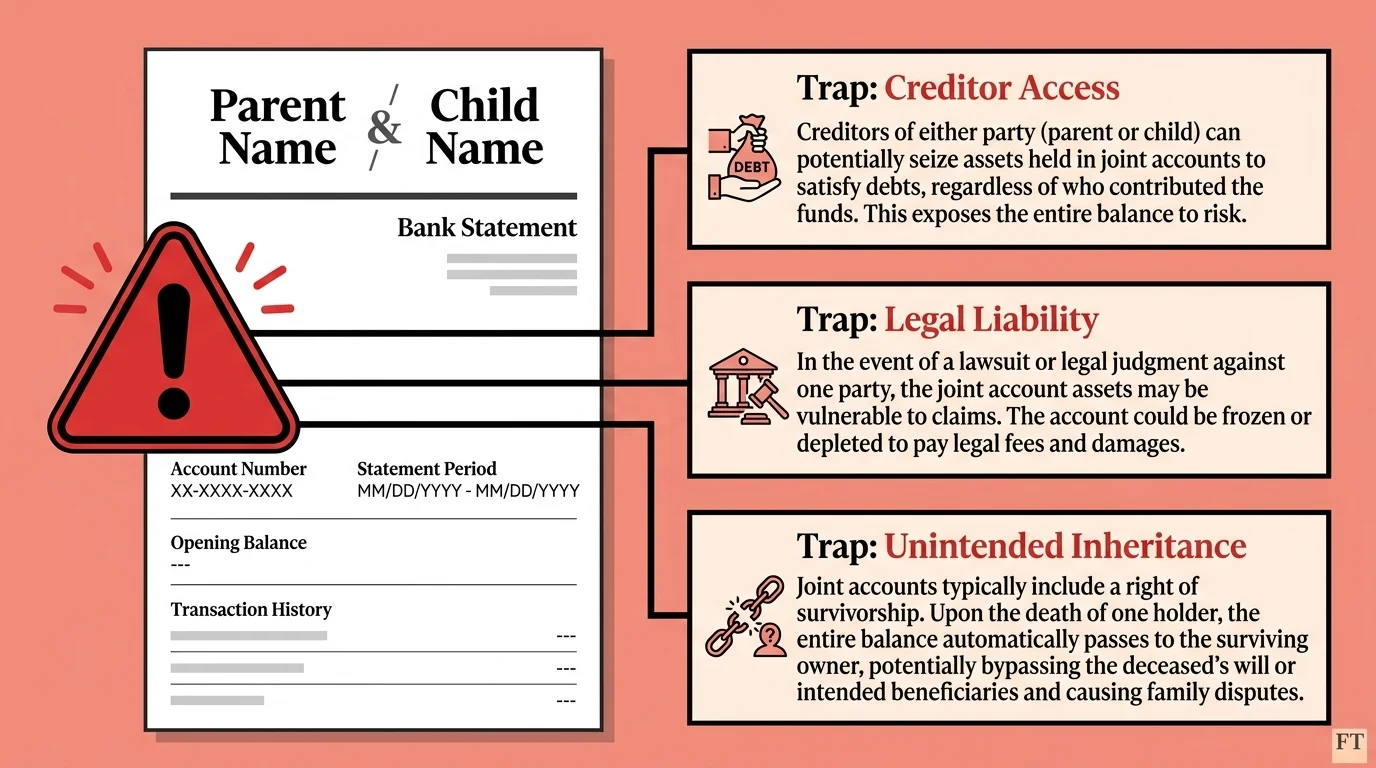

Mistake: The Joint Account Trap

In an effort to ensure seamless access to funds and bypass probate, aging parents frequently add an adult child as a joint owner on their primary checking or savings accounts. While this strategy seems wonderfully simple, it creates massive, often unforeseen liabilities. The moment you are added as a joint owner, those funds become legally yours as well. This means your parent’s life savings are suddenly exposed to your personal creditors. If you go through a contentious divorce, declare bankruptcy, or are found at fault in a major car accident, those joint funds can be seized to satisfy your debts.

Furthermore, when the parent passes away, the remaining funds in the joint account automatically belong entirely to the surviving joint owner. If the parent intended for that money to be split equally among three siblings, the joint owner has no legal obligation to share the cash. This scenario routinely destroys sibling relationships. Instead of joint ownership, parents should utilize payable-on-death designations and establish a durable power of attorney.

Mistake: Hiding the Original Documents

People naturally want to protect their most important legal paperwork, which often leads them to lock their original will and trust documents inside a bank safe deposit box. This creates a maddening catch-22. When the parent passes away, the bank typically seals the safe deposit box. The family cannot access the box without providing letters of testamentary from the probate court, but the family cannot get those letters from the court without presenting the original will trapped inside the box.

To avoid this administrative nightmare, keep the original documents in a fireproof, waterproof safe at home and ensure the named executor has the code or key. Alternatively, the attorney who drafted the documents can often hold the originals in their firm’s secure vault.

Mistake: Do-It-Yourself Legal Documents

The internet offers countless templates and software programs promising to generate cheap, instant legal documents. While these DIY tools might suffice for a young, single person with minimal assets, they are incredibly dangerous for older adults with established wealth, real estate, or complex family structures. DIY templates frequently fail to account for specific state laws, utilize ambiguous language, and lack the proper execution protocols—such as the correct number of witnesses or necessary notary seals. A document deemed invalid by a probate judge is worse than having no document at all, as it provides a false sense of security.

Mistake: Assuming Equal Means Fair

Parents generally default to splitting their assets equally among their children, assuming this represents the fairest approach. However, equality does not always equate to fairness or practicality. For instance, if one adult child has spent five years living with the parent, acting as their unpaid, full-time caregiver and sacrificing their own career progression, leaving the family home equally to all siblings might force the caregiver into homelessness when the house is sold to divide the proceeds.

Similarly, leaving a large lump sum of equal cash to a child with severe substance abuse issues or crippling debt is detrimental. Families must have honest conversations about the unique needs, contributions, and challenges of each child, and utilize mechanisms like trusts to protect vulnerable beneficiaries.