Common Mistakes and How to Avoid Them

Even cautious homeowners and drivers can fall into traps set by complex policy language and shifting industry standards. Avoiding the following critical errors will save you from devastating financial surprises.

Assuming Your Policy Will Automatically Renew

For decades, consumers paid their premiums and assumed their coverage would automatically roll over for another year. The 2026 insurance outlook in the US renders this assumption highly dangerous. Insurers are aggressively auditing their portfolios and dropping properties that no longer meet their strict profitability metrics. If a satellite image flags debris on your roof or an unpermitted trampoline in your yard, the company may issue a non-renewal notice without warning. You must open every piece of correspondence from your carrier immediately. Reviewing your policy well ahead of its expiration date gives you the crucial time needed to address maintenance issues or find alternative coverage.

Dropping Homeowners Insurance Completely

Faced with skyrocketing premiums that outpace inflation, a growing segment of the population has opted to drop their homeowners insurance entirely. Currently, roughly 12% of American homeowners are opting to go without coverage. This constitutes a catastrophic financial mistake. If a fire or severe storm destroys your uninsured home, you lose your primary asset and face potential bankruptcy trying to rebuild. Rather than abandoning your coverage, work with your agent to raise your deductible to the highest affordable level, drop non-essential riders, and ensure your core structure remains protected against a total loss.

Ignoring the Fine Print on Roof Coverage

Roofs represent the largest point of vulnerability for both homeowners and insurance companies. A common mistake involves assuming your standard policy will fully fund a brand-new roof after a hail storm. In response to massive weather-related losses, many carriers now strictly limit payouts for roofs older than ten to fifteen years, transitioning them from Replacement Cost Value to Actual Cash Value. This means the insurer deducts thousands of dollars for depreciation before issuing your check. You must read the specific endorsements attached to your policy; if your roof coverage has been downgraded, you need to begin aggressively saving for your inevitable replacement costs.

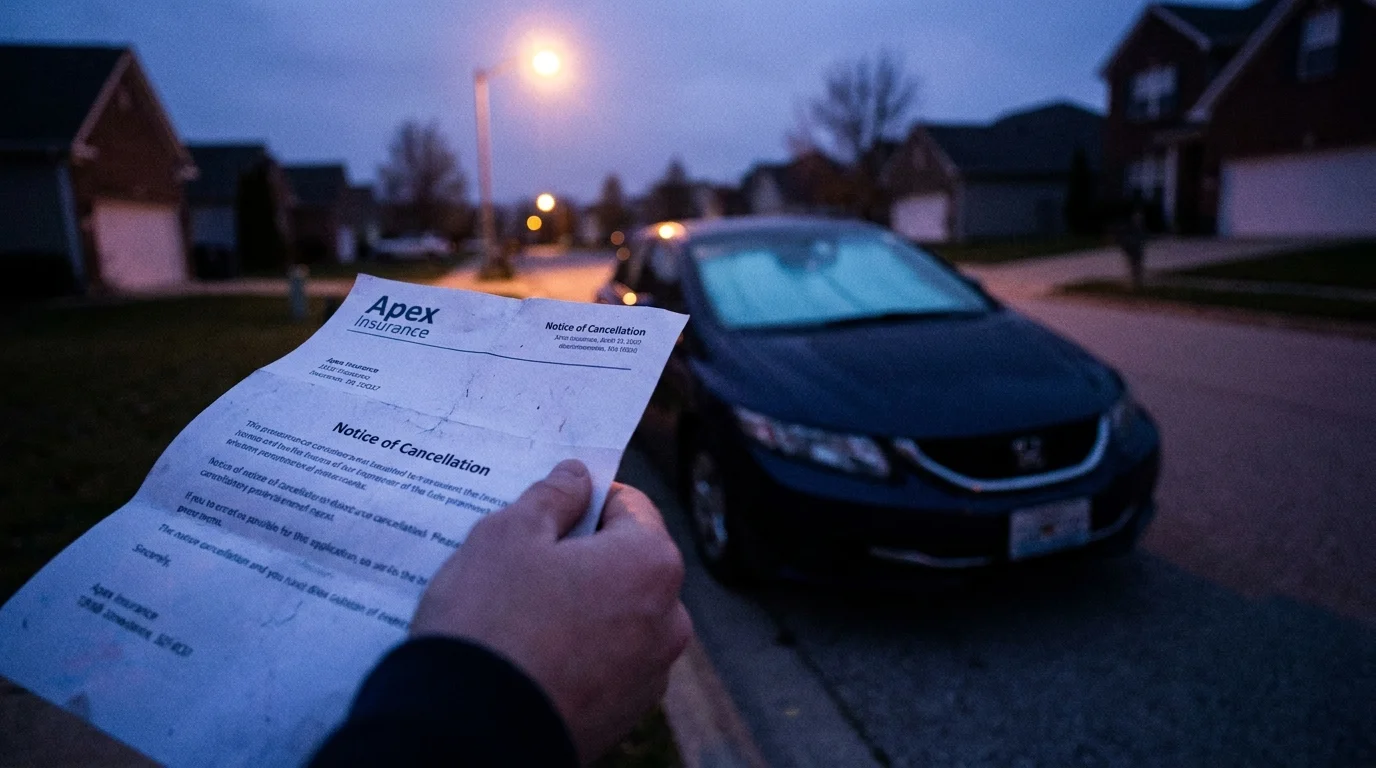

Letting Your Auto Insurance Lapse

In an effort to save money during a tough month, some drivers temporarily cancel their auto insurance with the intention of restarting it later. This strategy severely backfires. Insurance companies view continuous coverage as a primary indicator of responsibility. A lapse of even a few days categorizes you as a high-risk driver, triggering severe rate penalties when you attempt to secure a new policy. While some states have introduced protections preventing a first-time lapse from triggering a rate hike for drivers with long-term continuous coverage, the general rule remains unforgiving. If you need to reduce costs, lower your coverage limits temporarily rather than allowing your policy to lapse completely.