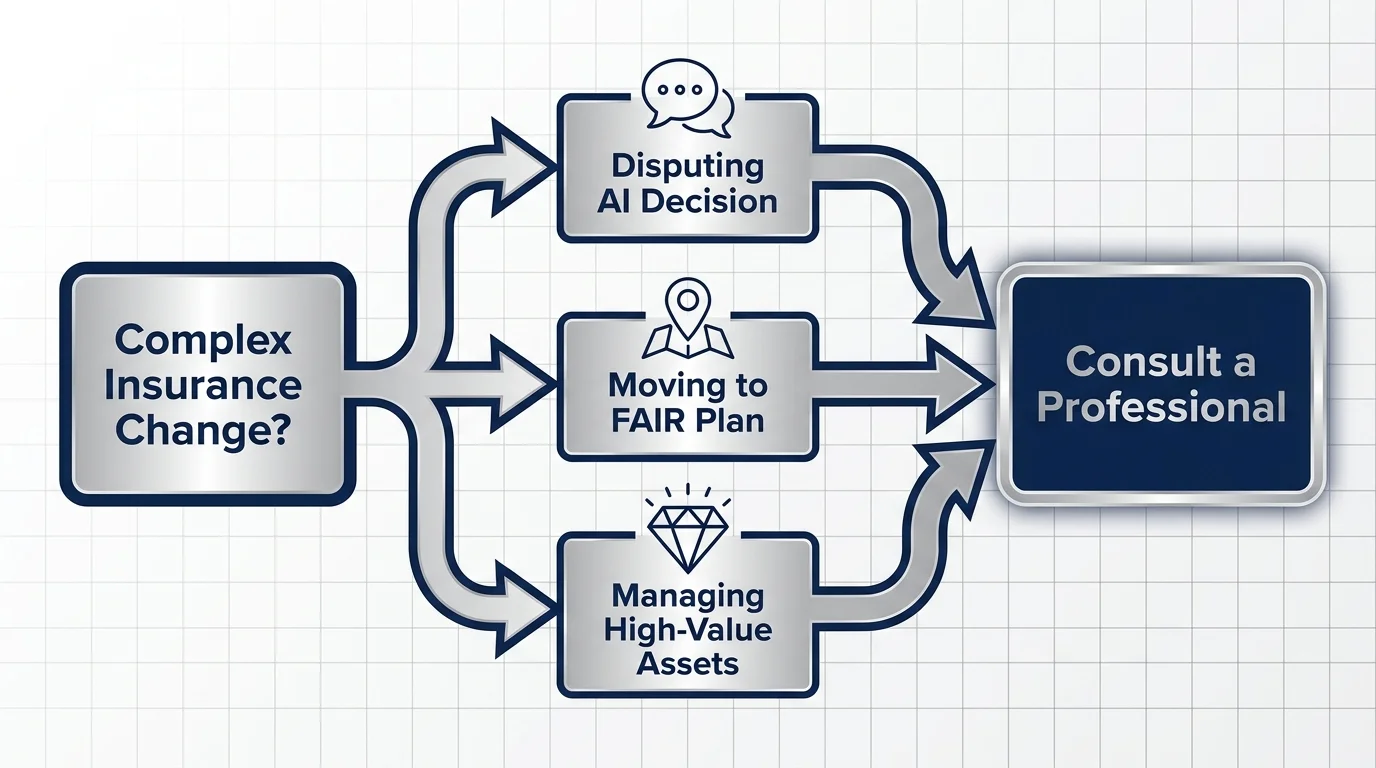

When to Consult a Professional

While you can manage basic policy adjustments on your own, certain situations require the expertise of a licensed professional. Knowing when to ask for help can mean the difference between robust protection and financial ruin.

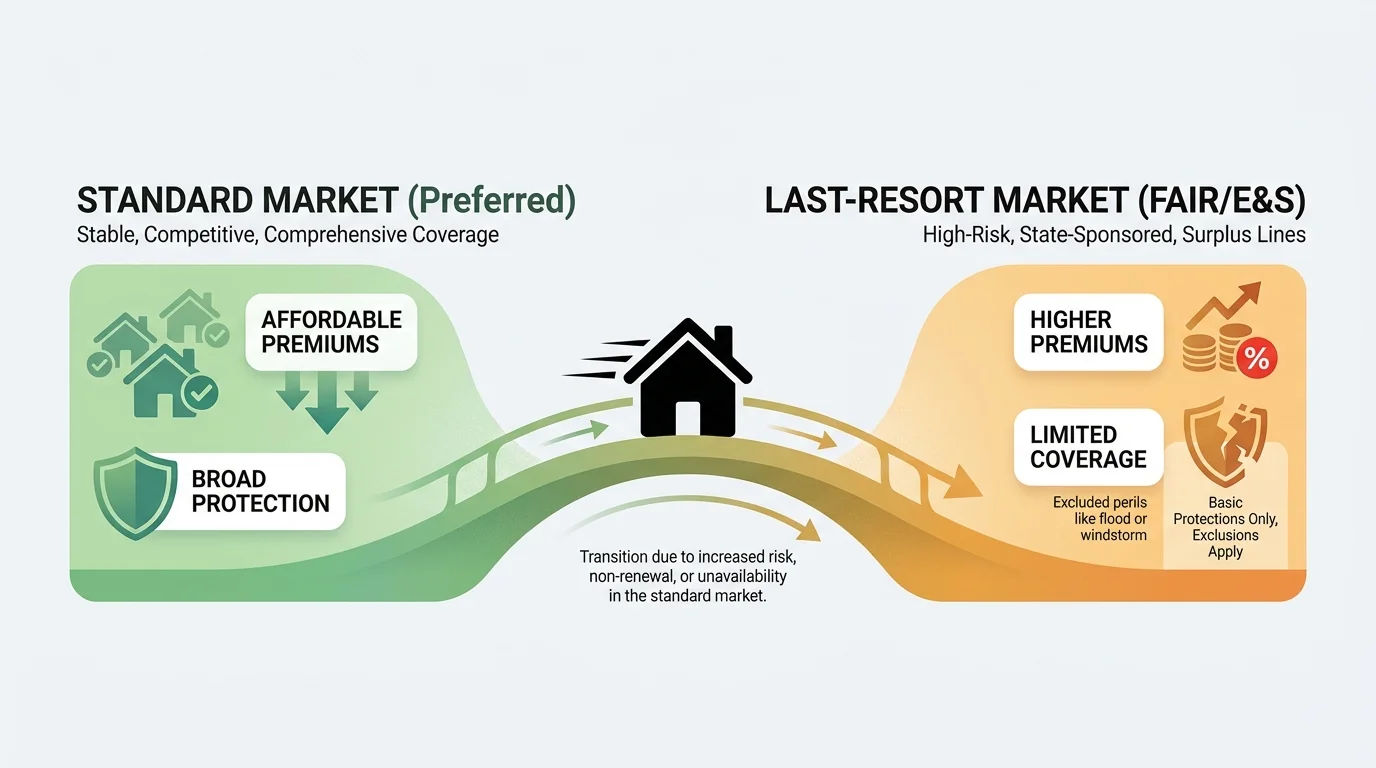

Transitioning to Last-Resort Coverage Options

If a standard carrier drops your homeowners policy due to wildfire or hurricane risks, navigating the transition to a state-backed FAIR plan or the Excess and Surplus market requires expert guidance. These alternative policies are notoriously complex and frequently exclude vital protections, such as liability coverage or water damage. An independent insurance broker understands the intricacies of these fragmented policies. They can help you piece together a comprehensive safety net by pairing a FAIR plan with supplementary difference in conditions policies, ensuring you do not encounter devastating coverage gaps when a disaster strikes.

Disputing AI-Driven Underwriting Decisions

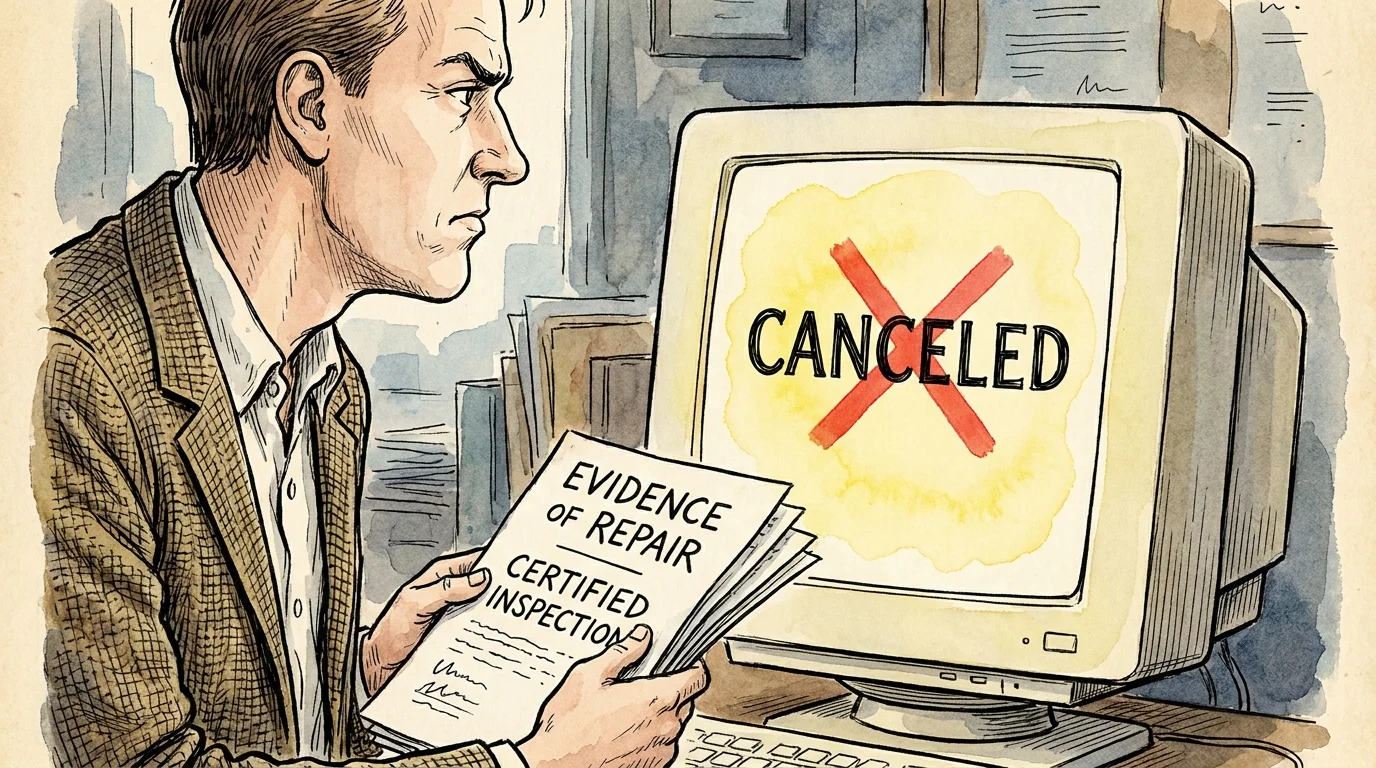

As the insurance industry aggressively scales its use of artificial intelligence and aerial surveillance, algorithmic errors frequently occur. A drone might mistake harmless shadows for severe roof damage, or an automated system might incorrectly classify your home’s proximity to a fire hydrant. If you receive a cancellation notice based on faulty automated data, do not accept the decision passively. Consult your insurance agent immediately. A dedicated professional knows how to formally dispute these assessments, request a manual underwriting review, and submit secondary proof—such as updated photos or contractor reports—to reverse an inaccurate cancellation.

Planning Major Lifestyle or Property Changes

Significant life events drastically alter your risk profile and insurance needs. If you are adding a newly licensed teenage driver to your auto policy, renovating your kitchen, installing a swimming pool, or launching a home-based business, your standard coverage will no longer suffice. Attempting to manage these updates through a generic online portal often results in inadequate protection. You should consult a specialized insurance advisor who can accurately assess your increased liability. They can recommend strategic solutions, such as securing a personal umbrella policy, which provides an extra layer of liability protection across both your home and auto exposures at a highly cost-effective rate.

Managing High-Value Assets in a Volatile Market

Standard insurance policies feature strict limits regarding the payout for luxury items, fine art, expensive jewelry, and custom vehicle modifications. As replacement costs surge due to inflation and supply chain constraints, your existing limits may fall dangerously short. High-net-worth individuals or those with unique property portfolios face exceptional challenges in the 2026 market. Consulting an agent who specializes in private client services ensures that your unique assets are appraised accurately and insured for their true replacement value. These professionals can secure specialized floaters and endorsements that generic carriers simply do not offer.