Helping your parents organize their final affairs gives your family clarity and protects their legacy from unnecessary legal hurdles. As parents approach their eightieth birthday, the risk of unexpected health crises increases dramatically; stepping in now ensures their wishes are honored and their assets are secure. You need to gather critical documents, understand financial accounts, and facilitate open conversations about their healthcare preferences. This proactive approach minimizes stress during emergencies and prevents costly delays in probate court. Taking the time to structure these details today provides everyone with profound peace of mind and preserves family harmony for the future.

Key Concepts and Terminology Explained

Understanding the vocabulary used by attorneys and financial advisors represents the crucial first phase of organizing your family finances. When you sit down to discuss these matters with your parents, knowing the correct terminology prevents confusion and helps you ask the right questions. Estate planning encompasses much more than simply deciding who receives a house or a bank account; it involves comprehensive preparation for medical emergencies, mental incapacity, and the eventual transfer of wealth.

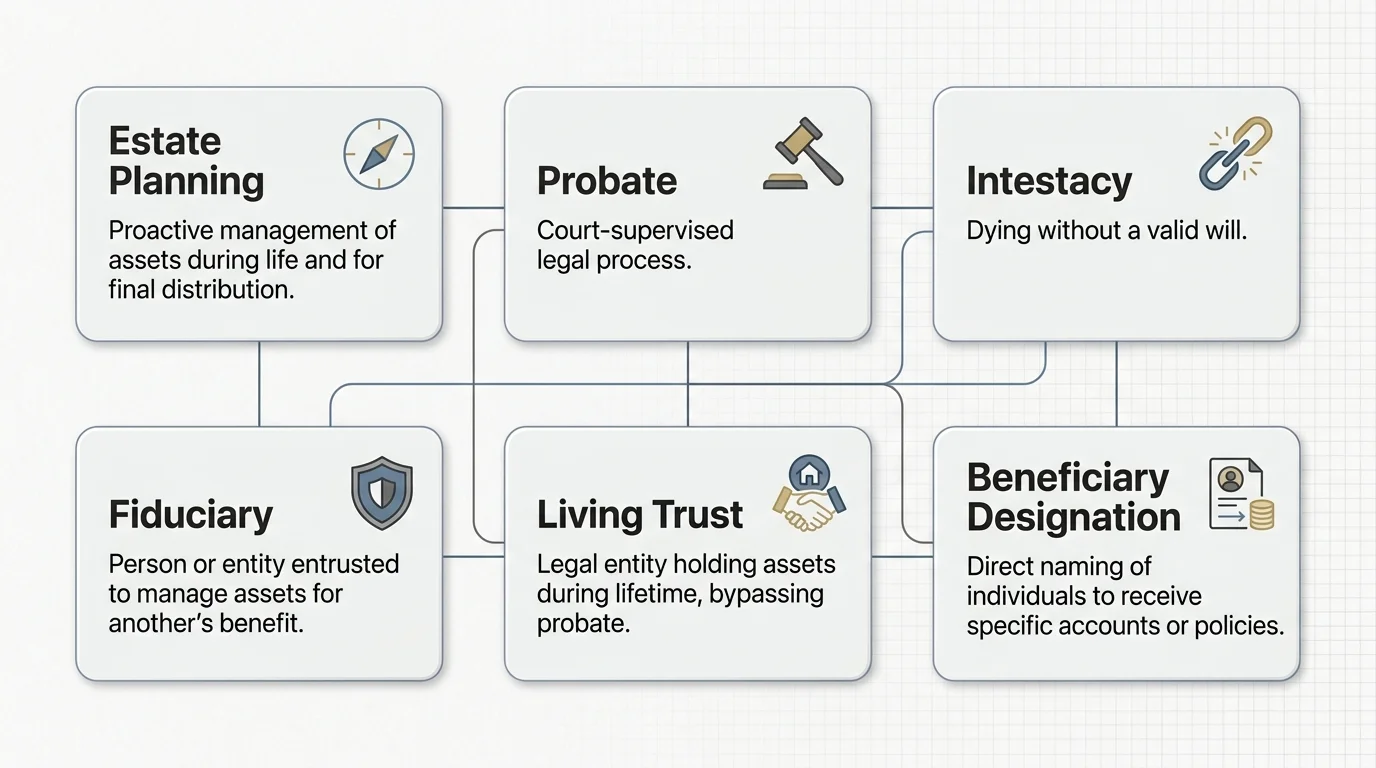

Estate Planning: This broad term refers to the deliberate process of anticipating and arranging for the management and disposal of a person’s estate during their life and after death. A comprehensive plan minimizes taxes, eliminates legal hurdles, and provides specific instructions for both healthcare and financial decisions.

Probate: Probate is the formal, court-supervised legal process of validating a deceased person’s will, paying off their outstanding debts, and distributing their remaining assets to the rightful heirs. Depending on the complexity of the estate and the specific laws of your state, probate can consume months or even years. It also generates public records, meaning anyone can see the details of your parent’s assets and inheritance distributions. Many families actively structure their plans to bypass probate entirely to save time, reduce legal fees, and maintain privacy.

Intestacy: If your parent passes away without a valid will or trust, they die intestate. In this scenario, state laws dictate how the assets are divided among surviving relatives. These rigid formulas do not account for personal relationships or informal promises, which often leads to unintended distributions and heated family disputes.

Fiduciary: A fiduciary is a person or organization legally bound to act in the best financial interest of another person. When your parents name an executor, a trustee, or an agent under a power of attorney, they are appointing a fiduciary. This individual must manage the assets responsibly and ethically, putting the parent’s interests above their own.

Living Trust: Unlike a will, a living trust is a legal entity created to hold ownership of an individual’s assets. The person creating the trust, known as the grantor, typically serves as the trustee during their lifetime, maintaining complete control over the property. Upon their death or incapacity, a designated successor trustee steps in to manage or distribute the assets according to the trust’s instructions. Crucially, assets held in a living trust completely bypass the probate process.

Beneficiary Designation: Certain financial accounts—such as life insurance policies, retirement accounts, and payable-on-death bank accounts—allow the owner to name a specific person to receive the funds immediately upon their death. These designations supersede any instructions written in a will. If a will states that all assets go to a current spouse, but a life insurance policy lists an ex-spouse as the beneficiary, the ex-spouse will receive the payout.