Protecting your family’s future requires more than just financial savings; it demands a clear, legally sound strategy to navigate unexpected life events. Establishing a comprehensive estate planning framework ensures your assets are distributed according to your wishes and relieves your loved ones from the burden of making difficult medical or financial decisions during a crisis. Without proper legal documents in place, state laws dictate who inherits your property and who manages your care, often leading to costly probate battles and family disputes. By organizing essential family law directives right now, you maintain control over your legacy and provide invaluable peace of mind to the people you cherish most.

Key Concepts and Terminology Explained

Before you begin drafting essential paperwork, you must understand the fundamental concepts that guide legal planning. The legal landscape relies heavily on highly specific terminology; familiarizing yourself with these phrases ensures you know exactly what rights you are transferring and what protections you are securing for your family. A strong foundational knowledge empowers you to make confident decisions when mapping out your future.

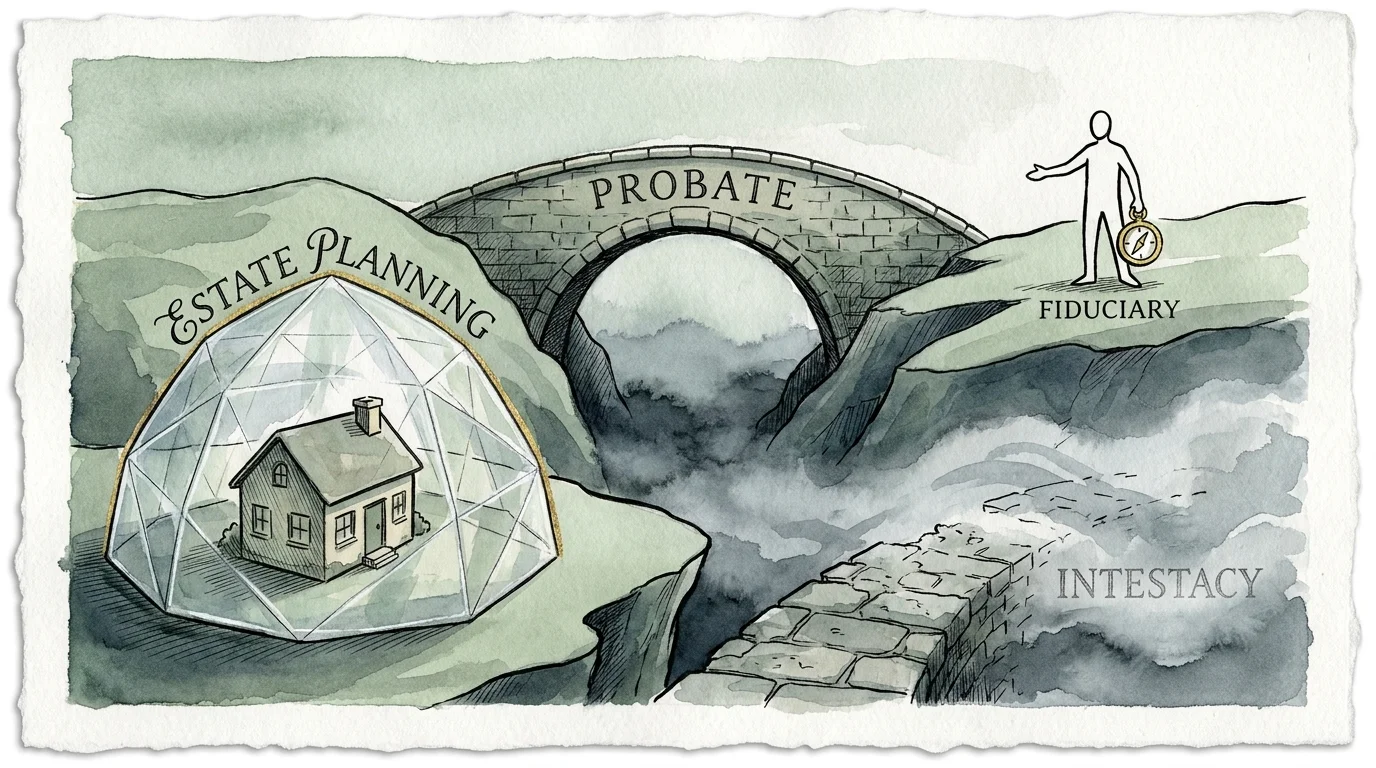

Estate Planning: This concept encompasses the comprehensive process of anticipating and arranging for the management and disposal of your estate during your life and after your death. Effective estate planning minimizes tax liabilities, outlines your healthcare preferences, and establishes a clear financial succession plan. More importantly, it secures your family’s financial stability and prevents unnecessary infighting among relatives.

Probate: Probate operates as the formal, court-supervised legal process that provides recognition to a will. During probate, a judge appoints an executor or personal representative who administers the estate, pays off outstanding debts, and distributes remaining assets to the intended beneficiaries. Because probate is a public record and often proves exceptionally time-consuming and expensive, many families focus their legal planning efforts on avoiding this court process entirely through trusts and specific account designations.

Fiduciary Duty: When you name someone to act on your behalf—such as an executor administering your will or an agent wielding a power of attorney—that individual becomes a fiduciary. A fiduciary is legally and ethically bound to act in your best financial and personal interest rather than their own. They must manage your affairs with prudence, loyalty, and strict adherence to your written instructions. If a fiduciary abuses this power or acts selfishly, they can face severe legal consequences and personal liability.

Intestacy: If you pass away without executing a valid will, you die “intestate.” When this happens, your local state government relies on default succession laws to distribute your property. Intestacy laws generally favor surviving spouses and direct descendants; however, these default rules rarely align perfectly with a person’s actual wishes. State laws do not account for complex family dynamics, stepchildren, unmarried partners, or close friends, meaning your closest loved ones could be left entirely disinherited.

Beneficiary: A beneficiary represents any person, charity, or legal entity you designate to receive the financial benefit of property you own. You can name beneficiaries within wills, living trusts, life insurance policies, and retirement accounts. Keeping your beneficiary designations completely updated serves as a critical component of family law and estate management, as these specific designations frequently override instructions left in a standard will.