A Practical Guide to Navigating Insurance Changes

With an understanding of the terminology, you can take decisive action to protect your assets. The 2026 insurance outlook in the US demands a proactive approach; simply paying your bills and hoping for the best is a strategy destined for failure.

Assess Your State’s Evolving Regulatory Standards

State governments regulate insurance, meaning your location dictates your rates and consumer protections. In 2026, numerous states have updated their laws to balance carrier solvency with consumer needs. For example, New Jersey finalized a transition requiring all drivers to carry increased minimum liability limits of $35,000 per person, $70,000 per accident, and $25,000 for property damage. Conversely, Louisiana enacted laws doubling the non-renewal notice period for home and auto policies to 60 days, while also prohibiting insurers from imposing rate hikes based on a single lapse in coverage. You must monitor your state’s Department of Insurance announcements so you can adapt your coverage limits to comply with the law.

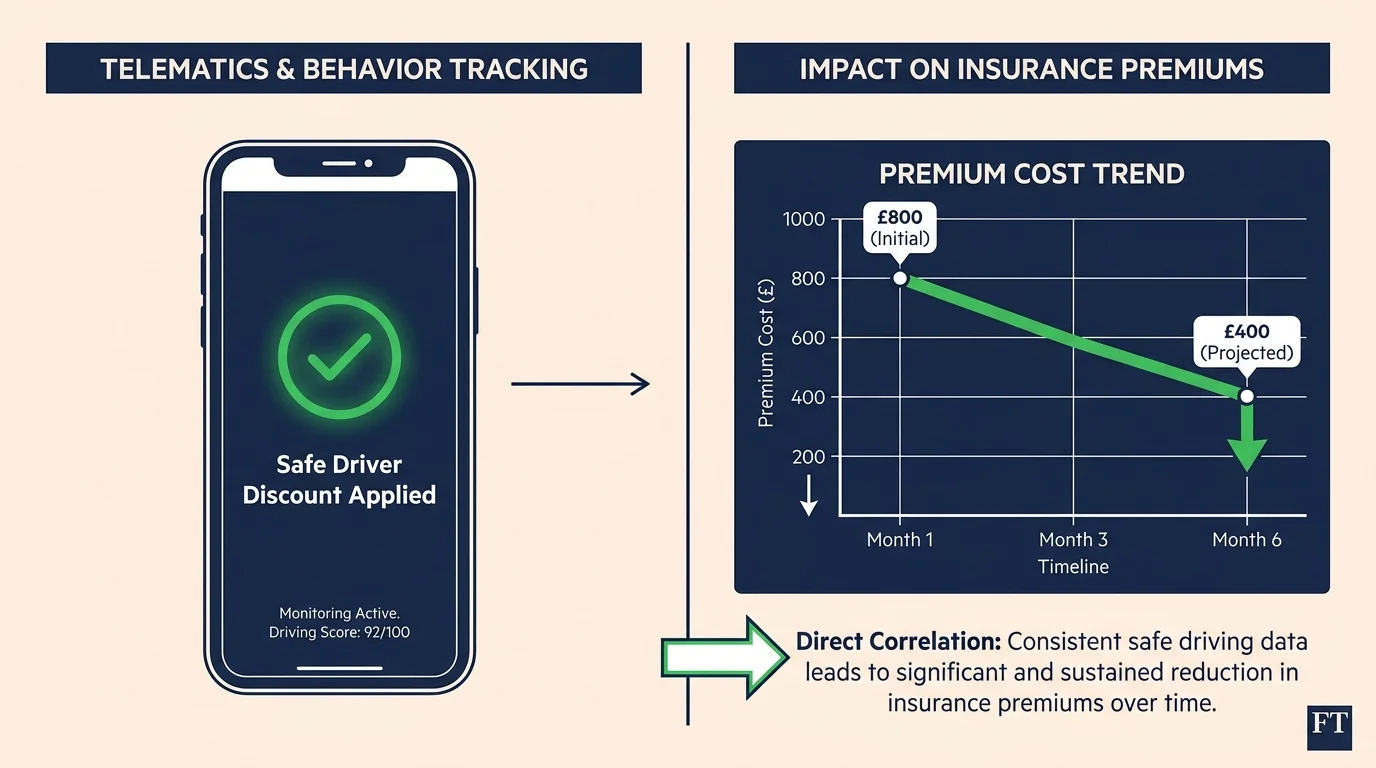

Leverage Telematics to Combat Rising Auto Premiums

The insurance trends defining 2026 indicate that the sharp, double-digit rate shocks of recent years are settling into a more moderate, mid-single-digit climb. However, baseline auto insurance rates in America remain historically high, driven by expensive vehicle repair costs, sophisticated car electronics, and elevated medical expenses. To offset these costs, you should evaluate usage-based insurance programs. Insurers grant their best rates to drivers who prove they present a low risk. Review the privacy policy of any telematics program carefully, but recognize that allowing your insurer to monitor your driving habits remains one of the few guaranteed strategies to lower your monthly bill.

Harden Your Home Against Climate Risks

Severe convective storms, wildfires, and flooding continuously disrupt the insurance market. Insurers frequently utilize drone imagery to decide whether to keep or drop your policy based on your property’s vulnerability. You can fight back by physically hardening your home. If you live in a fire-prone region, create defensible space by clearing brush and dead vegetation away from your structure. For wind and hail regions, consider upgrading to impact-resistant roofing materials or installing storm shutters. Keep detailed records and receipts of these upgrades. Presenting proof of a fortified home to your agent can secure critical discounts and prevent an unexpected non-renewal notice from arriving in your mailbox.

Shop the Market Ruthlessly and Strategically

Consumer loyalty no longer results in lower insurance premiums. In fact, many carriers rely on a loyalty penalty, quietly increasing rates on long-term customers who rarely check the competition. Recent data shows that shopping for auto and property insurance has surged to record highs, bucking traditional seasonal trends as people aggressively hunt for relief. You should engage an independent insurance agent to compare quotes across multiple carriers at least once every two years. An independent agent accesses dozens of companies, whereas a captive agent represents only one. You secure the best value by forcing companies to compete for your business.

Identify and Avoid Modern Insurance Fraud

As costs rise, fraudsters continuously invent new methods to exploit the system, which ultimately drives up premiums for everyone. Be deeply skeptical of ghost brokers who advertise impossibly cheap auto insurance rates on social media. These scammers provide forged insurance cards, take your money, and leave you entirely uninsured when an accident happens. Additionally, avoid engaging with aggressive legal solicitations that encourage you to exaggerate injuries after a minor fender bender; exaggerated claims and fraudulent lawsuits drain millions from the system annually, directly contributing to the heavy premiums burdening honest drivers across the country. Protect your personal information and only purchase policies from licensed, verified brokers.