Key Concepts and Terminology Explained

To successfully navigate the home and auto insurance changes in 2026, you first need to understand the evolving language of the industry. Insurance carriers have fundamentally updated how they assess risk, price their policies, and interact with consumers. Knowing these terms will help you decode your policy documents and have more productive conversations with your agent.

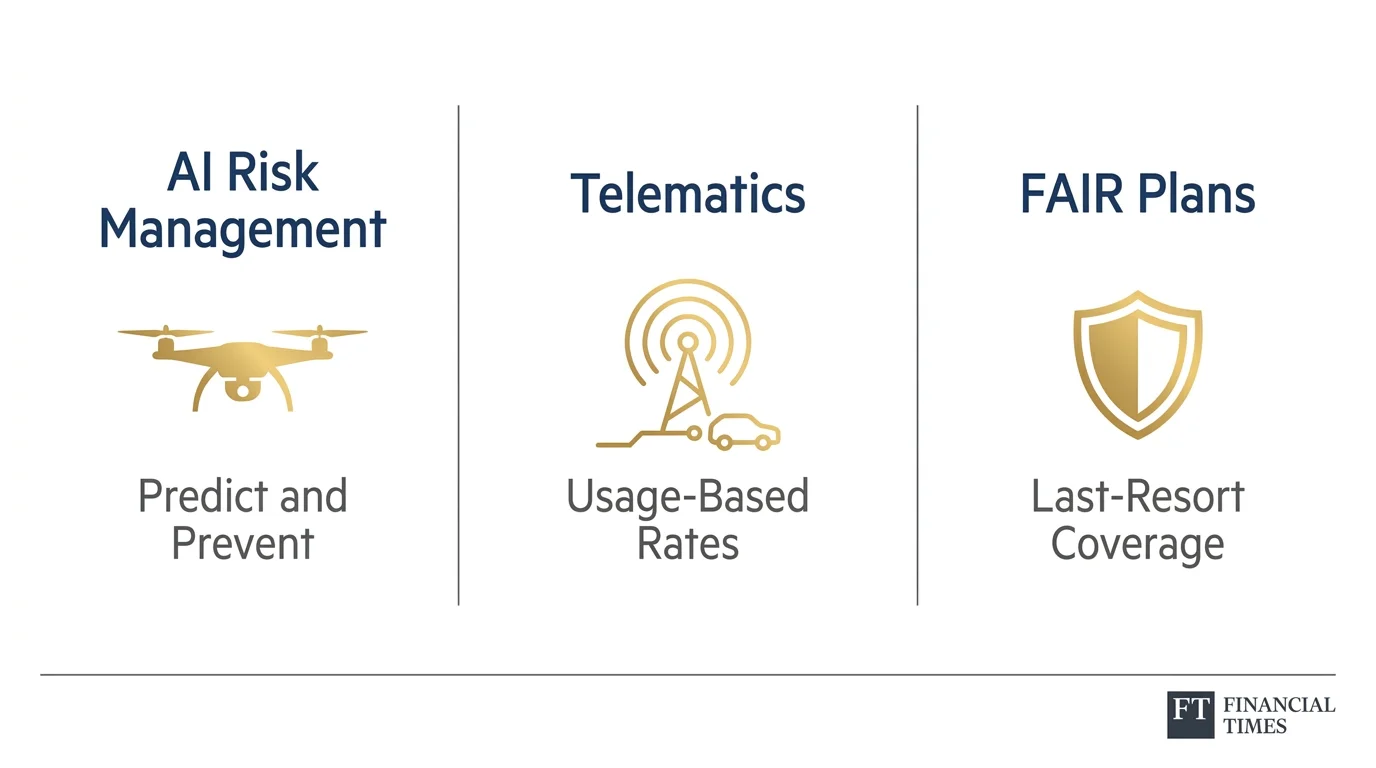

The Shift to Predict and Prevent Using Artificial Intelligence

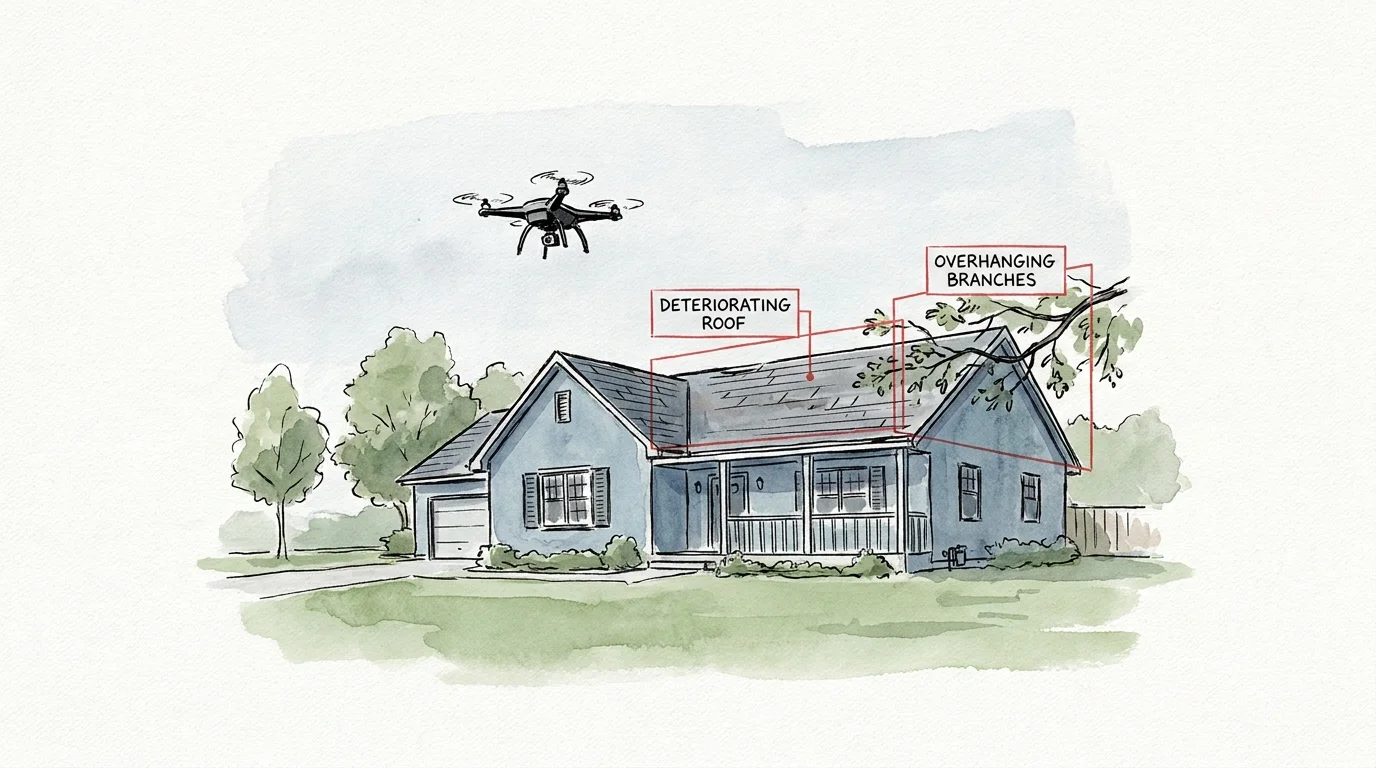

Insurers no longer wait for you to file a claim; they actively scan your life and property to predict risks. Companies utilize artificial intelligence to process satellite imagery and drone footage of your property before your policy renews. If an algorithm spots overhanging branches, a deteriorating roof, or clutter in your yard, the carrier may issue an ultimatum: fix the issue or face immediate cancellation. This marks a stark departure from the traditional model of simple risk transfer, replacing it with a hyper-vigilant standard of ongoing risk management. You must proactively maintain your home because an automated system is likely watching.

Telematics and Usage-Based Auto Insurance

Telematics involves the use of smartphone applications or small plug-in devices to track your real-time driving behavior. While insurers originally introduced these programs as optional ways to secure a discount, telematics has rapidly become a central pillar of the 2026 insurance rate forecast. Companies monitor your speed, hard braking, acceleration, phone usage, and late-night driving. Drivers who opt out of these tracking programs often find themselves placed in higher risk tiers by default. You trade a degree of personal privacy for the opportunity to control your insurance costs based on your actual habits behind the wheel.

State-Backed FAIR Plans and the Excess and Surplus Market

As mainstream carriers pull back from states prone to wildfires and hurricanes, millions of Americans have lost access to standard homeowners insurance. If a traditional company denies you coverage, you must turn to Fair Access to Insurance Requirements (FAIR) plans or the Excess and Surplus (E&S) market. FAIR plans serve as state-mandated insurers of last resort, offering basic, highly restricted coverage at premium prices. Alternatively, E&S carriers operate outside standard state regulations, allowing them to insure extreme risks while charging steep rates and imposing aggressive exclusions. If you live in California, Florida, or Texas, you are increasingly likely to encounter these fallback options.

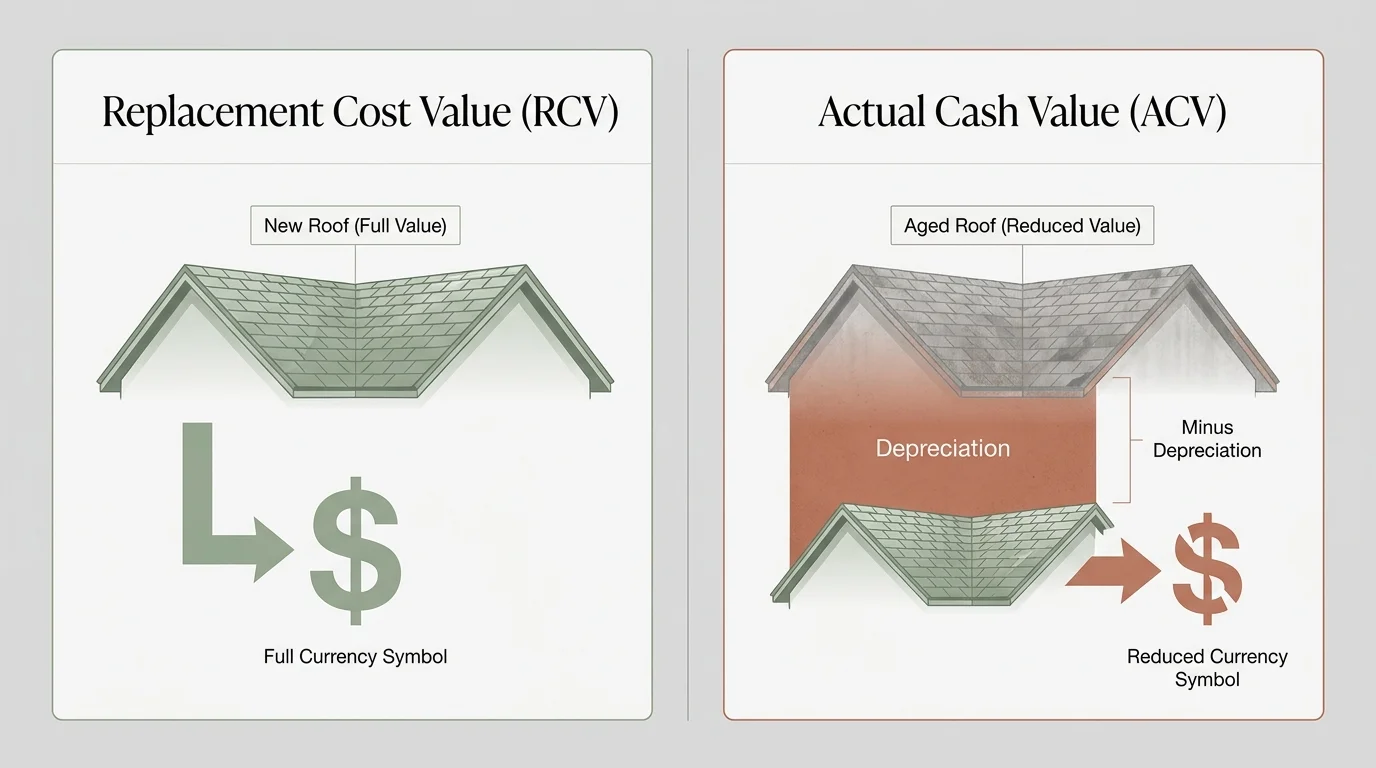

Actual Cash Value Versus Replacement Cost Value

Understanding how your insurer pays out a claim is more critical than ever, especially regarding your roof. Replacement Cost Value (RCV) covers the full expense of replacing your damaged property with new materials at today’s prices. Actual Cash Value (ACV), however, subtracts depreciation from the payout based on the age and condition of the item. In 2026, many carriers have quietly shifted older roofs to ACV schedules. If a severe storm destroys your fifteen-year-old roof, an ACV policy might only pay a fraction of the replacement cost, leaving you to cover a massive financial shortfall out of your own pocket.

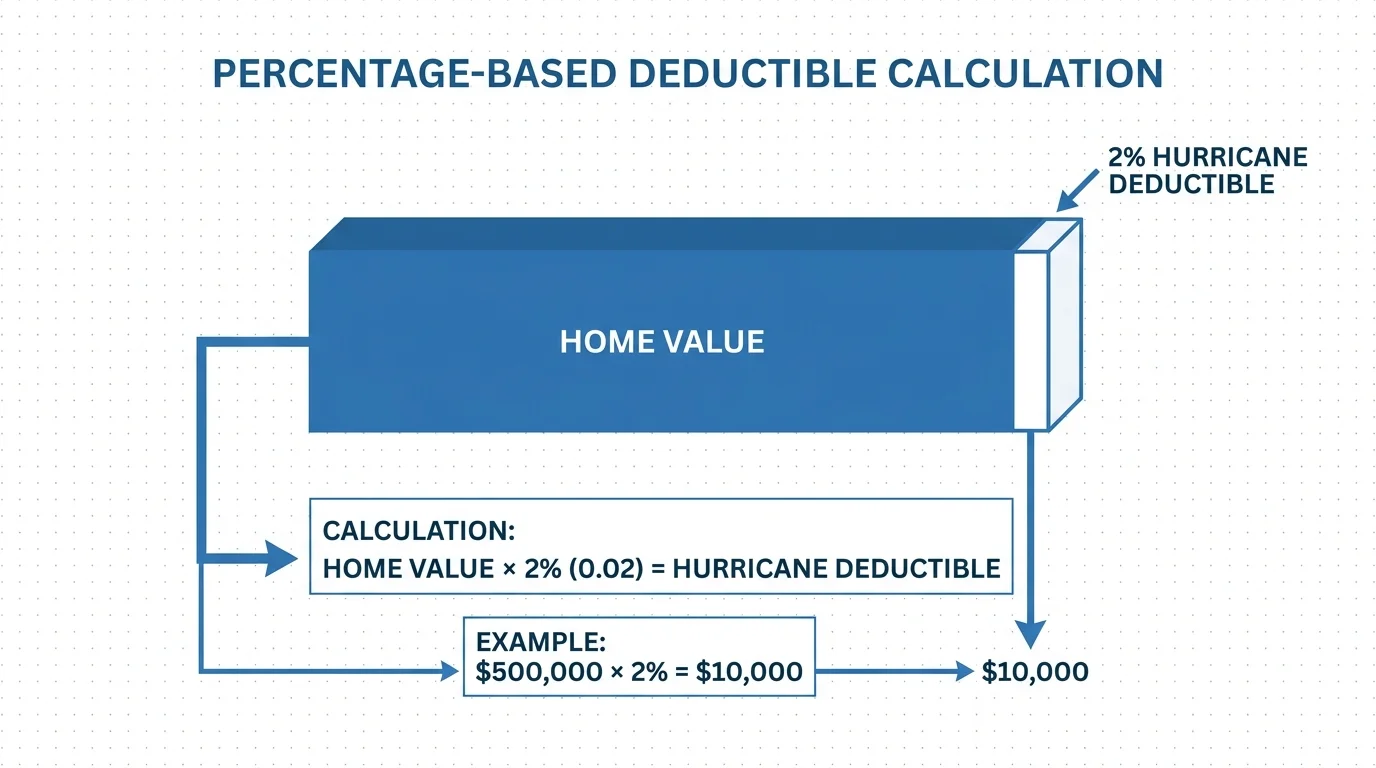

Percentage-Based Deductibles

In previous years, you likely had a flat-dollar deductible, such as $1,000, for any claim you filed. Today, insurers aggressively utilize percentage-based deductibles for specific perils like wind, hail, and hurricanes. A 2% wind deductible means you are responsible for 2% of your home’s total insured dwelling value, not a flat fee. If you insure your home for $400,000, a 2% deductible forces you to pay $8,000 before your coverage activates. You must read your declarations page carefully to identify these shifting financial burdens.