A Practical Guide to 8 Legal Myths Americans Still Believe

Countless individuals make poor financial and personal decisions based on inaccurate information they absorb from pop culture. Let us dismantle eight of the most prevalent legal myths and replace them with factual, actionable reality.

Myth 1: Verbal Contracts Are Completely Unenforceable

Many people assume that without a formally signed document, an agreement holds absolutely no legal weight. This pervasive myth leads individuals to make casual promises they later regret, believing they can simply walk away without consequences.

In reality, oral contracts hold significant legal weight in many daily transactions. If you agree to pay your neighbor five hundred dollars to paint your fence, and they complete the work based on your verbal promise, a valid contract exists. A court can, and often will, enforce that agreement. The primary challenge with verbal contracts lies in proving the terms of the agreement, not in their inherent validity. Judges frequently look at text messages, emails, witness testimony, and the subsequent actions of both parties to determine what was promised.

However, the law does mandate written contracts for specific, high-stakes transactions under a doctrine known as the Statute of Frauds. These exceptions generally include the sale of real estate, agreements that take longer than one year to fulfill, and promises to pay someone else’s debt. To protect yourself, always document your agreements. Even a simple email summarizing a verbal conversation creates a powerful paper trail.

Myth 2: If You Die Without a Will, the State Seizes Your Entire Estate

Fear often drives estate planning, and one of the most common fears involves the government swooping in to confiscate a family’s wealth. People frequently believe that dying without a will—known as dying intestate—automatically transfers all their money and property directly to the state treasury.

This scenario rarely happens. When you die without a will, your state’s intestate succession laws take effect. These laws act as a default estate plan, directing your assets to your closest living relatives. The exact distribution varies by state, but the hierarchy generally prioritizes your surviving spouse and children. If you have no spouse or children, the court looks for your parents, then siblings, then nieces and nephews, and continues down the family tree.

The state only claims your assets—a process called “escheatment”—if the probate court exhausts every avenue and cannot locate a single living blood relative. While the state rarely takes your money, dying intestate still causes massive headaches. It strips you of the ability to choose your beneficiaries, name guardians for your minor children, or leave money to a charity or an unmarried partner.

Myth 3: Undercover Police Officers Must Identify Themselves if Asked

Decades of television crime dramas have convinced the American public that undercover police officers face a strict legal obligation to reveal their true identity if directly asked. The myth suggests that if an officer lies about being a cop, any subsequent arrest qualifies as illegal entrapment.

This represents a complete fiction. Law enforcement officers legally possess the right to lie about their identity during an investigation. If an undercover officer had to admit their profession every time a suspect asked, undercover operations would instantly collapse, placing officers in severe danger. The legal concept of entrapment requires much more than simple deception. Entrapment only occurs when a police officer coerces, forces, or overwhelmingly persuades someone to commit a crime they otherwise had absolutely no intention of committing.

Merely providing a suspect with the opportunity to break the law—such as offering to buy stolen goods while posing as a criminal—does not constitute entrapment. You should never rely on the “are you a cop” question to protect yourself from legal consequences.

Myth 4: Moving to Another State Erases Your Unpaid Debts

Individuals drowning in consumer debt sometimes view a cross-country move as a clean slate. They believe that if they relocate to a different state, collection agencies and creditors lose the authority to pursue them for old credit card balances, medical bills, or personal loans.

Debt does not respect state lines. The American financial system relies on highly integrated, national credit reporting bureaus—Equifax, Experian, and TransUnion. When you default on a debt in New York, it instantly damages your credit profile in California. Furthermore, creditors possess the legal tools to chase you across the country. If a creditor sues you and wins a judgment in your old state, they can easily “domesticate” that judgment in your new state. This process allows them to garnish your new wages or place a lien on your new property, exactly as they would have done before you moved.

Instead of attempting to outrun your financial obligations, you must confront them directly. Negotiating payment plans, seeking credit counseling, or consulting a bankruptcy professional offer practical, legally sound methods for handling overwhelming debt.

Myth 5: Employers Need a Legally Valid Reason to Fire You

Many workers assume that their employer must provide a justifiable, documented reason—such as poor performance, chronic tardiness, or misconduct—before terminating their employment. This belief leads to intense shock and confusion when employees face sudden dismissal without explanation.

As previously established, the vast majority of the American workforce operates under the doctrine of at-will employment. Your employer can legally fire you because they dislike your attitude, because they want to hire their nephew, or simply because it is a Tuesday. They do not need to provide you with a warning, put you on a performance improvement plan, or offer a good reason, provided their motivation is not inherently illegal.

The law only intervenes when an employer fires someone for a discriminatory reason protected by federal or state law. You cannot be fired based on your race, gender, religion, national origin, age, or disability. Additionally, employers cannot fire you in retaliation for reporting illegal activity, taking protected family leave, or refusing to perform an unsafe act. Unless you belong to a union or hold a specific employment contract, your job security relies heavily on your employer’s discretion.

Myth 6: “Finders Keepers” Protects You When You Keep Discovered Property

The childhood playground rule of “finders keepers, losers weepers” does not translate into adult legal reality. Many people believe that if they find a wallet on the street, a laptop in a coffee shop, or a valuable piece of jewelry in a public park, they possess the legal right to claim ownership after a brief waiting period.

The law treats found property very carefully, distinguishing between lost, mislaid, and abandoned items. If you find a wallet full of cash on the sidewalk, the law considers it “lost” property. The original owner did not intend to part with it. You hold a legal obligation to make a reasonable attempt to locate the true owner, often by turning the item over to the local police department. If you simply pocket the wallet and spend the cash, you commit theft, technically known as “theft by finding” or “larceny.”

Property is only considered “abandoned”—meaning you can legally claim it—if the original owner clearly intended to discard it, such as leaving a piece of furniture on the curb with a “free” sign. When in doubt about discovered valuables, involving local law enforcement protects you from criminal liability.

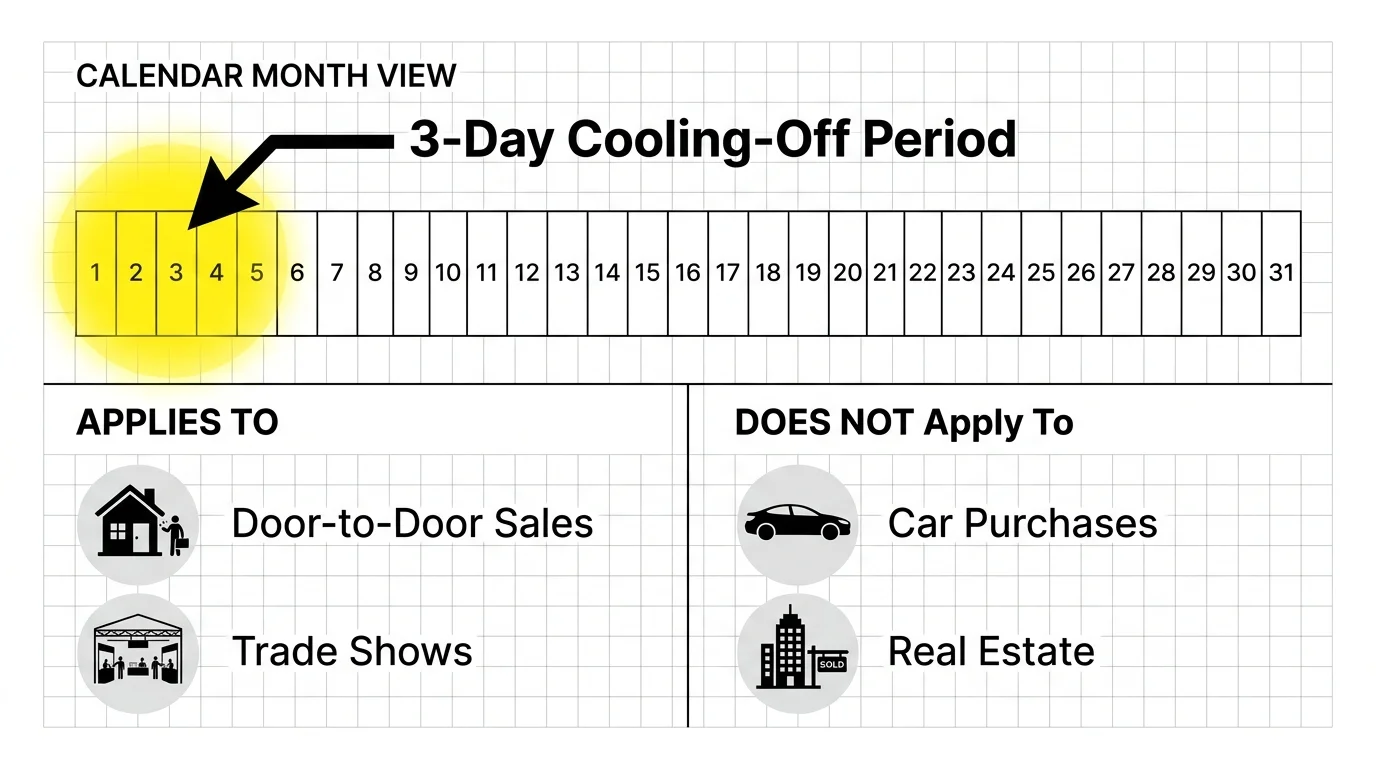

Myth 7: A Three-Day “Cooling-Off” Period Applies to Every Major Purchase

Consumers frequently assume they possess an absolute, unconditional right to return a new vehicle or cancel an expensive contract within three days of signing. This persistent belief leads buyers to make impulsive decisions, assuming they can simply back out if they experience buyer’s remorse the following morning.

This myth stems from a massive oversimplification of the Federal Trade Commission’s (FTC) Cooling-Off Rule. The actual rule applies only to very specific types of transactions. It primarily protects consumers from high-pressure sales tactics occurring outside of a seller’s normal place of business. For example, you have three days to cancel a contract signed with a door-to-door salesperson, or an agreement made at a temporary trade show or hotel convention room.

Crucially, the FTC’s Cooling-Off Rule does not apply to vehicles purchased at a traditional auto dealership, standard retail purchases made at a brick-and-mortar store, or real estate transactions. Once you sign the paperwork at a car dealership and drive off the lot, you own that vehicle. Always read return policies and contract cancellation clauses meticulously before signing, rather than relying on a non-existent universal grace period.

Myth 8: Hiring an Attorney Always Requires a Massive Upfront Payment

The fear of exorbitant legal fees prevents countless Americans from seeking justice or protecting their rights. People picture writing a ten-thousand-dollar retainer check just to speak with an attorney, causing them to abandon valid legal claims or attempt dangerous do-it-yourself strategies in court.

While corporate litigation and complex criminal defense do require substantial retainers, many legal fields operate on highly accessible payment structures. Personal injury lawyers, workers’ compensation attorneys, and medical malpractice specialists almost universally work on a contingency fee basis. This means you pay nothing upfront; the lawyer only collects a fee—typically a percentage of the settlement—if they successfully win your case. If you lose, you owe them nothing for their time.

Furthermore, attorneys handling routine matters like drafting a standard will, reviewing a lease agreement, or forming a small business LLC often charge predictable flat fees rather than open-ended hourly rates. Legal aid societies and pro bono clinics also provide free or reduced-cost services to individuals facing financial hardship. You should never assume legal representation remains completely out of reach without first consulting a professional about their fee structures.