A Practical Guide to the Essential Legal Documents

Securing your financial and personal future requires a cohesive strategy. The following six documents form the foundation of a robust estate plan. Each serves a distinct purpose, and together, they ensure comprehensive protection for your golden years.

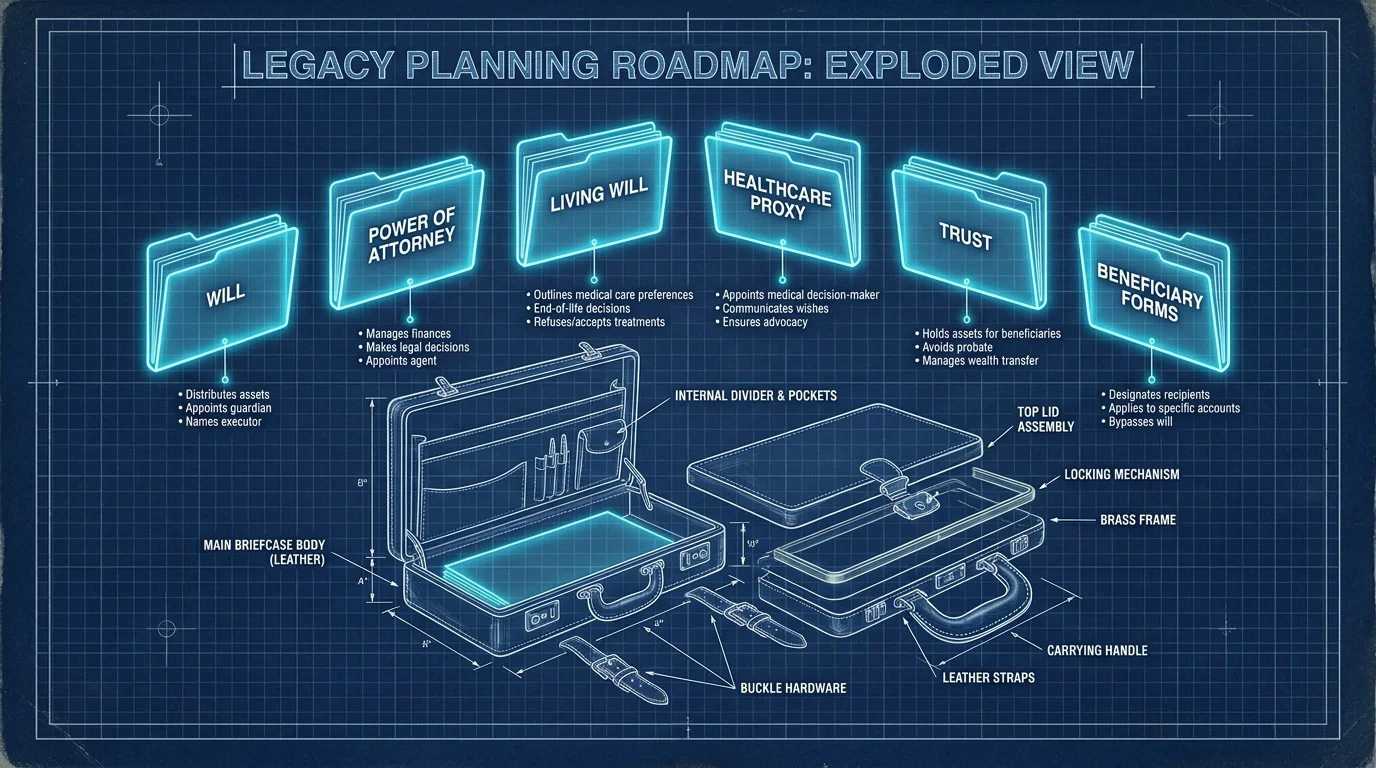

1. Last Will and Testament

Your last will and testament is the cornerstone of your estate plan. This document provides explicit instructions on how you want your assets distributed after your passing. It allows you to name an executor—the trusted individual responsible for managing your estate, paying off your final debts out of your assets, and distributing the remainder to your designated heirs.

From a financial perspective, a carefully drafted will prevents costly family disputes. Consider a scenario where a parent leaves behind a family home but has three adult children. Without a will dictating whether the house should be sold and the proceeds divided, or bought out by one sibling, the family might face expensive litigation. A will also allows you to make specific bequests, such as leaving a set monetary amount to a favorite charity or ensuring a beloved grandchild receives funds specifically designated for their college education.

Remember that a will only takes effect after you pass away, and it must go through the probate process. Even though it goes through the courts, having a will drastically simplifies and accelerates probate compared to dying intestate.

2. Durable Financial Power of Attorney

While a will details what happens after you die, a power of attorney protects you while you are still alive. A durable financial power of attorney designates a trusted agent to manage your financial affairs if you become incapacitated due to illness, injury, or cognitive decline. The word “durable” is vital; it means the document remains valid even after you lose the mental capacity to make decisions.

Financially, this is arguably the most critical document you can possess. If you suffer a severe stroke and lose your ability to communicate, your bills do not magically pause. Property taxes come due, mortgage payments must be made, and retirement distributions must be managed. If you lack a durable financial power of attorney, your family must petition a court to establish a conservatorship or guardianship. This legal proceeding is notoriously slow, expensive, and deeply invasive. Meanwhile, your financial life stalls. Your agent, armed with a power of attorney, can seamlessly interface with banks, sign tax returns, and protect your credit score from devastation during your recovery.

3. Advance Healthcare Directive (Living Will)

A living will—often referred to as an advance healthcare directive—outlines your specific wishes regarding end-of-life medical care. It provides clear instructions to medical professionals about the treatments you want and the ones you refuse if you are in a terminal condition or a permanent vegetative state.

You use a living will to clarify your stance on artificial nutrition, hydration, ventilator use, and cardiopulmonary resuscitation (CPR). By documenting these deeply personal choices in advance, you lift a massive emotional weight off your family’s shoulders. When families are forced to guess what a parent would have wanted, the resulting guilt and disagreement can fracture relationships forever. A living will ensures your voice is heard, preserving your dignity and sparing your loved ones from making agonizing, permanent decisions in the dark.

4. Medical Power of Attorney (Healthcare Proxy)

While a living will provides written instructions for end-of-life scenarios, it cannot possibly cover every medical situation. A medical power of attorney (also known as a healthcare proxy or healthcare surrogate) allows you to name a specific person to make real-time medical decisions for you if you cannot communicate them yourself.

Your medical proxy coordinates with your doctors, reviews your medical charts, decides on surgical interventions, and chooses which care facilities are best for your rehabilitation. You should select someone who is calm under pressure, who deeply understands your values, and who possesses the emotional fortitude to enforce your wishes—even if other family members disagree. Many seniors choose a spouse or an adult child, but the most important qualification is unwavering trustworthiness.

5. Revocable Living Trust

For seniors looking to optimize their financial legacy, a revocable living trust is a powerful alternative or supplement to a standard will. A trust is a legal entity that you create to hold ownership of your assets. Because it is “revocable,” you maintain complete control over the trust during your lifetime; you can add assets, remove assets, change the terms, or dissolve the trust entirely at your discretion.

The primary financial advantage of a living trust is probate avoidance. Assets held in the trust bypass the public, time-consuming probate court process entirely. Upon your passing, your designated successor trustee immediately steps in and distributes the assets to your beneficiaries according to your private instructions. This uninterrupted transition saves your estate thousands of dollars in court fees and prevents public snooping into your family’s financial affairs.

Furthermore, a living trust provides exceptional protection during incapacitation. If you develop dementia or face a severe health crisis, your successor trustee can seamlessly take over managing the assets within the trust to pay for your care, entirely avoiding the need for a court-appointed conservator.

6. HIPAA Authorization Form

The Health Insurance Portability and Accountability Act (HIPAA) enforces strict privacy rules that prevent medical professionals from sharing your health information with unauthorized individuals. While these privacy laws protect you from identity theft and employer discrimination, they create massive hurdles during a family medical emergency.

If you are rushed to the emergency room, doctors may legally refuse to discuss your condition, your prognosis, or your treatment plan with your children unless they have explicit authorization. A HIPAA release form is a simple document that lists the specific people who are legally allowed to receive your medical information. You can sign a standalone HIPAA authorization or incorporate it directly into your medical power of attorney. Ensuring this document is on file guarantees your family stays informed when minutes matter most.