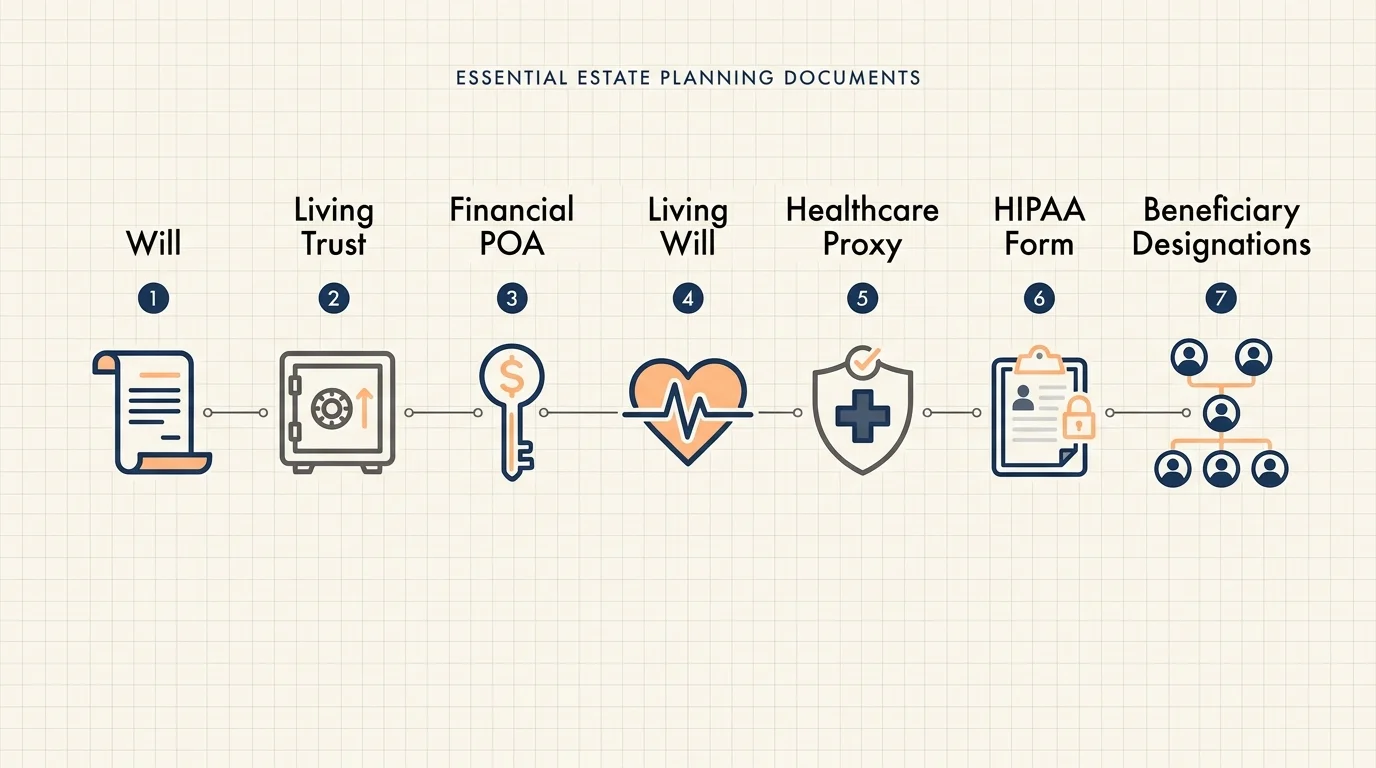

A Practical Guide to 7 Legal Documents Every Family Should Have Ready

Every household faces unique financial circumstances and personal dynamics, yet the foundational elements of asset protection and healthcare delegation remain remarkably universal across the board. The following seven legal documents form the bedrock of a secure, comprehensive family plan. Implementing these tools ensures that your assets, medical care, and loved ones remain protected regardless of what unexpected challenges the future holds.

1. The Last Will and Testament

The last will and testament serves as the most widely recognized component of any estate plan. This foundational document allows you to explicitly state how you want your physical assets, real estate, and financial accounts distributed after your passing. Without a valid will, you surrender all control over your legacy to your state’s default legal statutes. Through your will, you officially appoint an executor—a trusted individual tasked with gathering your assets, paying your final debts, and ensuring your exact distribution wishes are honored.

Beyond simple asset distribution, a will provides the exclusive legal mechanism for parents of minor children to nominate legal guardians. If you and your spouse pass away simultaneously without naming a guardian, a family court judge will decide who raises your children. The court may select a family member you would have strongly opposed, or worse, place your children in the state care system while relatives battle over custody. By establishing a will, you unequivocally define your preferences for your children’s upbringing, education, and living situation.

2. Revocable Living Trust

While a will directs your assets after death, a revocable living trust provides a robust mechanism to manage your property both during your lifetime and after your passing. When you establish a living trust, you legally transfer the ownership of your assets—such as your home, investment accounts, and valuable personal property—into the trust’s name. You remain the primary trustee, meaning you retain complete control over these assets while you are alive and capable. You can spend the money, sell the property, or dissolve the trust entirely at your discretion.

The primary advantage of a revocable living trust lies in its ability to completely bypass the probate process. When you pass away, the successor trustee you appointed seamlessly steps in to manage or distribute the trust’s assets to your beneficiaries without requiring any court intervention. This rapid transition saves your family thousands of dollars in legal fees, keeps your financial affairs entirely private, and provides your loved ones with immediate access to crucial funds during a difficult grieving period. Furthermore, trusts allow you to set specific conditions on inheritances, such as holding funds until a young beneficiary reaches a certain age or graduates from college.

3. Durable Financial Power of Attorney

Estate planning focuses heavily on end-of-life scenarios, but you must also prepare for the very real possibility of temporary or permanent incapacitation. A durable financial power of attorney authorizes a trusted individual—your agent—to manage your financial affairs if an illness, injury, or cognitive decline renders you unable to handle them yourself. The term “durable” holds profound importance; it signifies that the document remains legally valid and active even after you lose mental capacity.

Your agent can execute a wide variety of essential tasks on your behalf. They can access your bank accounts to pay your mortgage, manage your investment portfolios, file your state and federal taxes, and ensure your utility bills remain current. Without a durable financial power of attorney in place, your family members cannot simply step in and access your solely owned accounts. They would instead face the daunting task of petitioning a court for formal conservatorship—an expensive, stressful, and heavily monitored legal proceeding that can take months to resolve while your financial obligations pile up.

4. Advance Healthcare Directive (Living Will)

An advance healthcare directive, commonly referred to as a living will, explicitly outlines your personal preferences for end-of-life medical care. This document serves as your voice when severe trauma or terminal illness prevents you from communicating with your medical team. Within a living will, you provide specific instructions regarding extraordinary life-sustaining treatments, including the use of mechanical ventilators, artificial nutrition and hydration via feeding tubes, dialysis, and cardiopulmonary resuscitation (CPR).

Creating a detailed living will constitutes an act of profound compassion for your family. When sudden medical crises strike, families often experience paralyzing guilt and intense conflict over how to proceed with medical care. By documenting your exact wishes regarding quality of life and palliative care, you remove the burden of these agonizing choices from your spouse and children. They will not have to guess what you would have wanted; they simply follow the explicit, legally binding roadmap you left behind.

5. Healthcare Power of Attorney (Healthcare Proxy)

While a living will dictates your wishes for specific end-of-life scenarios, a healthcare power of attorney appoints a specific person to make active, real-time medical decisions on your behalf. This individual, known as your healthcare proxy or surrogate, collaborates directly with your doctors to manage your treatment plan whenever you cannot consent to care yourself. This document covers situations beyond just end-of-life care; your proxy can authorize surgical procedures, select rehabilitation facilities, and manage medication regimens if you are temporarily incapacitated due to an accident or severe illness.

You must select a proxy who possesses the emotional resilience to enforce your medical wishes, even if other family members disagree with the course of action. Your chosen representative should deeply understand your values, your religious beliefs regarding medical care, and your personal thresholds for acceptable quality of life. Empowering the right person ensures you receive the exact care you desire while preventing hospital staff from receiving conflicting demands from divided family members.

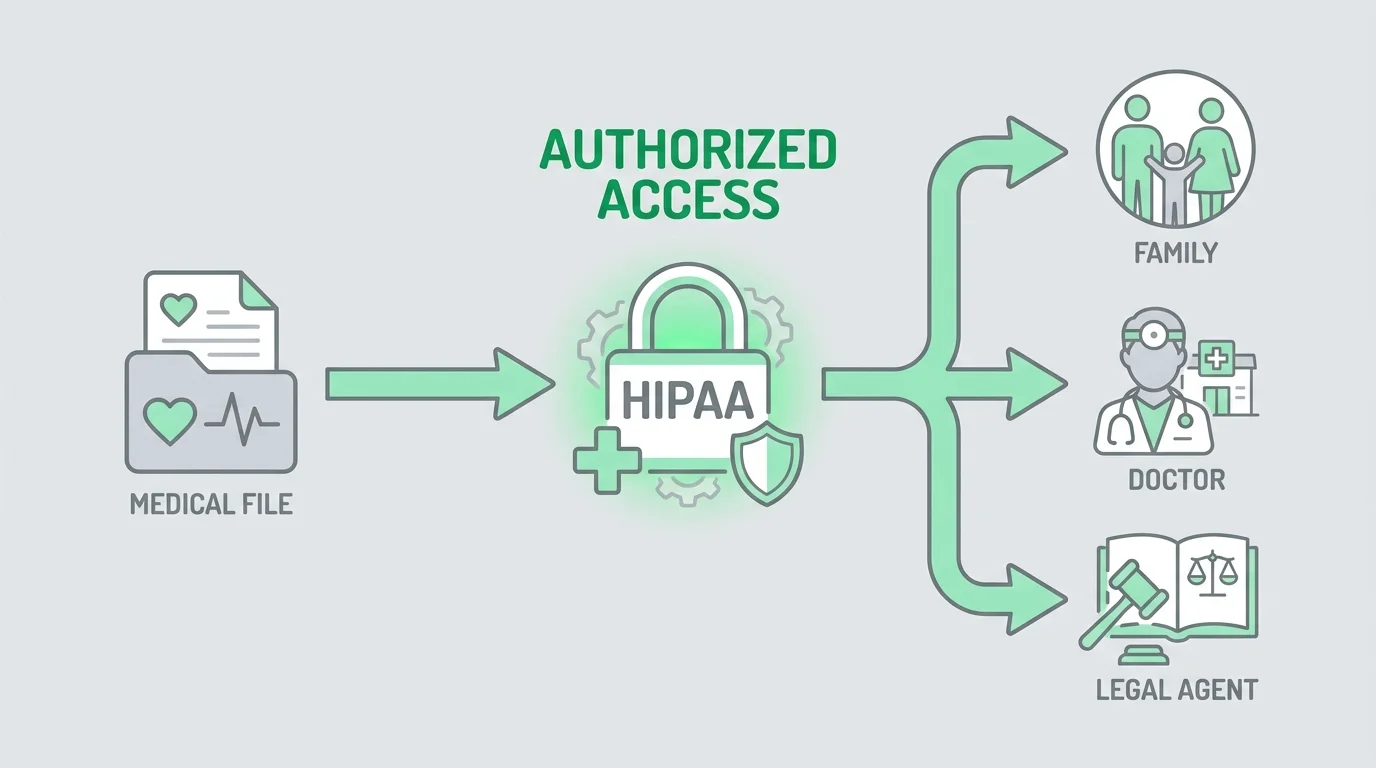

6. HIPAA Authorization Form

The Health Insurance Portability and Accountability Act (HIPAA) enforces strict federal privacy standards designed to protect your sensitive medical information. While these privacy laws protect you from unauthorized data breaches, they can severely obstruct your family’s ability to gather critical information during an emergency. Without a signed HIPAA authorization form, medical professionals face severe legal penalties for discussing your condition, prognosis, or treatment options with anyone—even your spouse or adult children.

A HIPAA authorization acts as a companion document to your healthcare power of attorney. It explicitly lists the individuals who have the legal right to receive updates about your health status and access your medical records. By signing this release in advance, you ensure your trusted loved ones can speak freely with your medical team, understand your current condition, and coordinate your recovery plan without facing frustrating bureaucratic blockades at the hospital front desk.

7. Beneficiary Designations

Many individuals mistakenly believe their last will and testament dictates the distribution of all their assets. In reality, specific financial accounts utilize beneficiary designations that legally override any instructions written in your will. Life insurance policies, 401(k) retirement plans, Individual Retirement Accounts (IRAs), and bank accounts with Payable-on-Death (POD) or Transfer-on-Death (TOD) provisions pass directly to the named beneficiaries outside of the probate process.

You establish these designations by filling out forms provided directly by your financial institutions. Because these designations operate independently of your formal estate plan, you must exercise extreme vigilance in keeping them updated. If you update your will to leave your entire estate to your current spouse but fail to remove your ex-spouse as the primary beneficiary on your life insurance policy, the insurance company will legally disburse the payout to your ex-spouse upon your death. Routinely auditing these designations ensures your most valuable liquid assets transfer to the correct individuals.