Common Mistakes and How to Avoid Them

Many families assume that once they sign their initial stack of legal documents, their estate planning responsibilities end. However, life remains dynamic; your financial portfolio, family structure, and personal preferences will inevitably evolve over time. Failing to treat your estate plan as an adaptable, living framework represents one of the most frequent pitfalls individuals encounter. Recognizing and avoiding these common errors preserves the integrity of your legal strategy.

Failing to Update Documents After Major Life Events

Your legal documents capture your wishes at a single point in time, but major life milestones drastically alter your priorities. Events such as marriage, divorce, the birth of a child, the death of a designated fiduciary, or a significant relocation to a new state all demand an immediate review of your estate plan. If you fail to update your will or powers of attorney after a divorce, your former spouse may retain the legal authority to make your medical decisions or inherit your hard-earned assets. You should institute a personal policy to review all legal documents every three to five years, or immediately following any major change in your family structure.

Relying Exclusively on Generic DIY Templates

The internet offers countless cheap, fill-in-the-blank legal templates that promise a quick fix for estate planning. While these templates may seem appealing for simple situations, they frequently fail to account for state-specific legal nuances and specific family complexities. A generic will might lack the precise witness signatures required by your state legislature, rendering the entire document legally void during probate. Furthermore, DIY templates rarely provide the customized language necessary to manage blended families, unique business assets, or specific tax reduction strategies. Cutting corners with unverified forms often ends up costing your family significantly more in litigation and probate fees down the road.

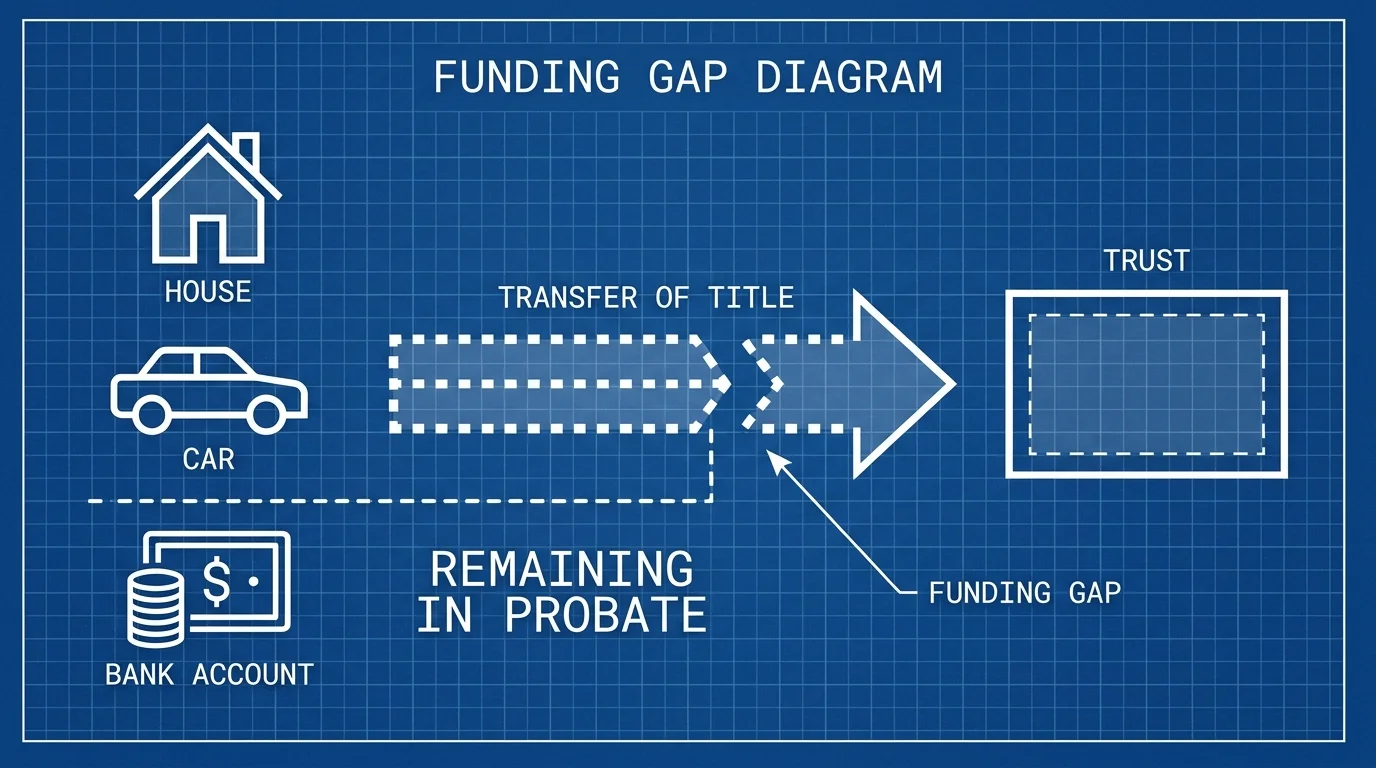

Failing to Actually Fund the Trust

Drafting and signing a revocable living trust document only completes the first half of the process; you must then physically transfer your assets into the trust to activate its protections. This critical step, known as “funding the trust,” requires you to retitle your home, update your bank account ownership, and reassign your investment portfolios into the name of the trust. If you sign the trust paperwork but leave your home deeded in your individual name, that property will still be forced through the sluggish probate process when you pass away. You must rigorously follow through on changing property titles and account ownership to reap the benefits of trust-based planning.

Hiding Documents and Failing to Communicate

The most flawlessly drafted estate plan provides zero protection if no one knows it exists or where to find it. Many individuals place their original documents inside a bank safe deposit box, only for their family to discover they lack the legal authority to access the box after a death or incapacitation occurs. You must store your original legal documents in a secure, fireproof location at home and explicitly communicate this location to your executor and chosen agents. Furthermore, engaging in transparent conversations with your family about your final wishes and medical preferences eliminates surprises, mitigates resentment, and ensures your fiduciaries feel confident stepping into their assigned roles.