A Practical Guide to 7 Legal Loopholes That Regular Americans Use

Everyday families utilize legal tips and statutory incentives to protect their wealth and reduce their tax liabilities. You do not need a team of corporate lawyers to take advantage of these allowances; you simply need an understanding of how the rules work. Below are seven practical strategies you can explore to optimize your financial standing.

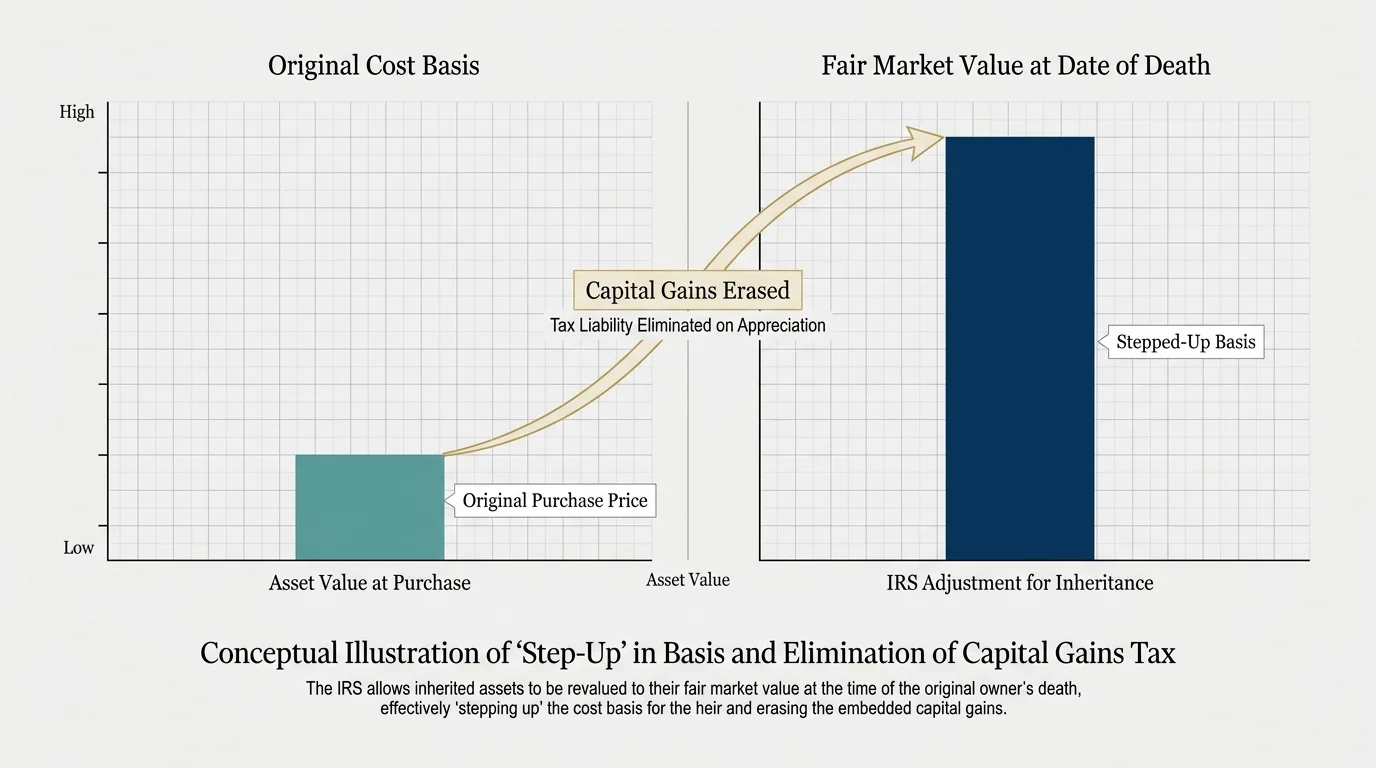

1. The Step-Up in Basis for Inherited Assets

One of the most powerful wealth-preservation tools in the tax code is the step-up in basis. When you inherit an asset, such as a family home or a stock portfolio, the Internal Revenue Service (IRS) adjusts the cost basis of that asset to its fair market value on the date of the original owner’s death. This adjustment effectively erases all the capital gains that accumulated during the deceased person’s lifetime.

Consider a practical example. Suppose your parents purchased a home thirty years ago for $50,000. Today, that home is worth $500,000. If they sell the home while they are alive, they might owe significant capital gains taxes on the $450,000 profit. Furthermore, if they simply sign the deed over to you as a gift while they are living, you inherit their original $50,000 cost basis. If you later sell the house for $500,000, you will owe taxes on the $450,000 gain.

However, if your parents hold onto the property and pass it to you through their estate after they die, your cost basis “steps up” to the current market value of $500,000. If you sell the home shortly thereafter for $500,000, your taxable capital gain is zero. Families use this loophole to transfer wealth across generations without losing massive portions of their estate to taxes.

2. The Augusta Rule (Section 280A)

The Augusta Rule, officially found in Section 280A of the Internal Revenue Code, allows homeowners to rent out their primary residence for up to 14 days per calendar year without reporting the rental income on their tax returns. The nickname stems from residents of Augusta, Georgia, who historically rented out their homes to wealthy visitors during the annual Masters golf tournament.

You can leverage this loophole if you live near a major annual event—such as a popular music festival, a professional sports championship, or a major convention. If you charge $1,000 a night and rent your home for 10 days, you collect $10,000 of entirely tax-free income. You do not need to report it, and the IRS does not tax it.

Small business owners take this a step further. If you own a legitimate business (such as an LLC or S-Corporation), your business can rent your home for a corporate retreat, a board meeting, or an extended planning session. The business gets to deduct the rental cost as a legitimate operating expense, and you, as the homeowner, receive the rental income tax-free, provided the arrangement does not exceed the 14-day annual limit and the rent charged reflects fair market value.

3. Tax-Loss Harvesting

Investing involves inevitable fluctuations. Savvy investors use market downturns to their advantage through a strategy called tax-loss harvesting. This loophole allows you to sell investments that have lost value to offset the taxes you owe on investments that have gained value.

If you sell a stock and realize a $10,000 capital gain, the IRS expects a percentage of that profit. However, if you also hold a different stock that has dropped in value by $10,000, you can sell the losing stock to realize the loss. The $10,000 loss cancels out the $10,000 gain, leaving you with zero net taxable capital gains for the year.

Even if you do not have capital gains to offset, the IRS allows you to apply up to $3,000 of capital losses against your ordinary income (such as your salary) each year. If your total losses exceed both your capital gains and the $3,000 ordinary income limit, you can carry the remaining losses forward to offset taxes in future years. This turns a bad investment decision into a valuable tax deduction.

4. Homestead Exemptions

Homestead exemptions represent a crucial category of asset protection laws designed to keep families from losing their primary residences to sudden financial ruin. When you declare your home as your primary residence (your “homestead”), state laws shield a specific amount of the equity in that home from unsecured creditors.

If you face a devastating lawsuit, massive medical bills, or credit card debt leading to bankruptcy, creditors typically attempt to liquidate your assets to satisfy the debts. Homestead laws prevent them from forcing the sale of your home, provided your equity falls within the state’s statutory limits.

These laws vary drastically by location. Some states offer relatively small protections, shielding only $15,000 to $30,000 of home equity. Conversely, states like Florida and Texas offer virtually unlimited homestead protection. In these jurisdictions, individuals can protect millions of dollars in home equity from unsecured creditors, making the homestead exemption a foundational pillar of their personal finance strategy.

5. Spousal IRA Contributions

Typically, the IRS requires you to have earned income—such as wages or a salary—to contribute to an Individual Retirement Account (IRA). This rule previously penalized single-income households, leaving stay-at-home parents unable to build tax-advantaged retirement accounts in their own names. The spousal IRA exception closes this gap.

Under this legal provision, a non-working spouse can open and fully fund a Traditional or Roth IRA based entirely on the working spouse’s income. If a married couple files a joint tax return, they can contribute to two separate IRAs, doubling their annual tax-advantaged retirement savings.

This ensures that stay-at-home partners can build independent wealth and take advantage of compounding interest over decades. It also provides the household with greater flexibility during retirement, as both partners will have distinct accounts from which to draw funds.

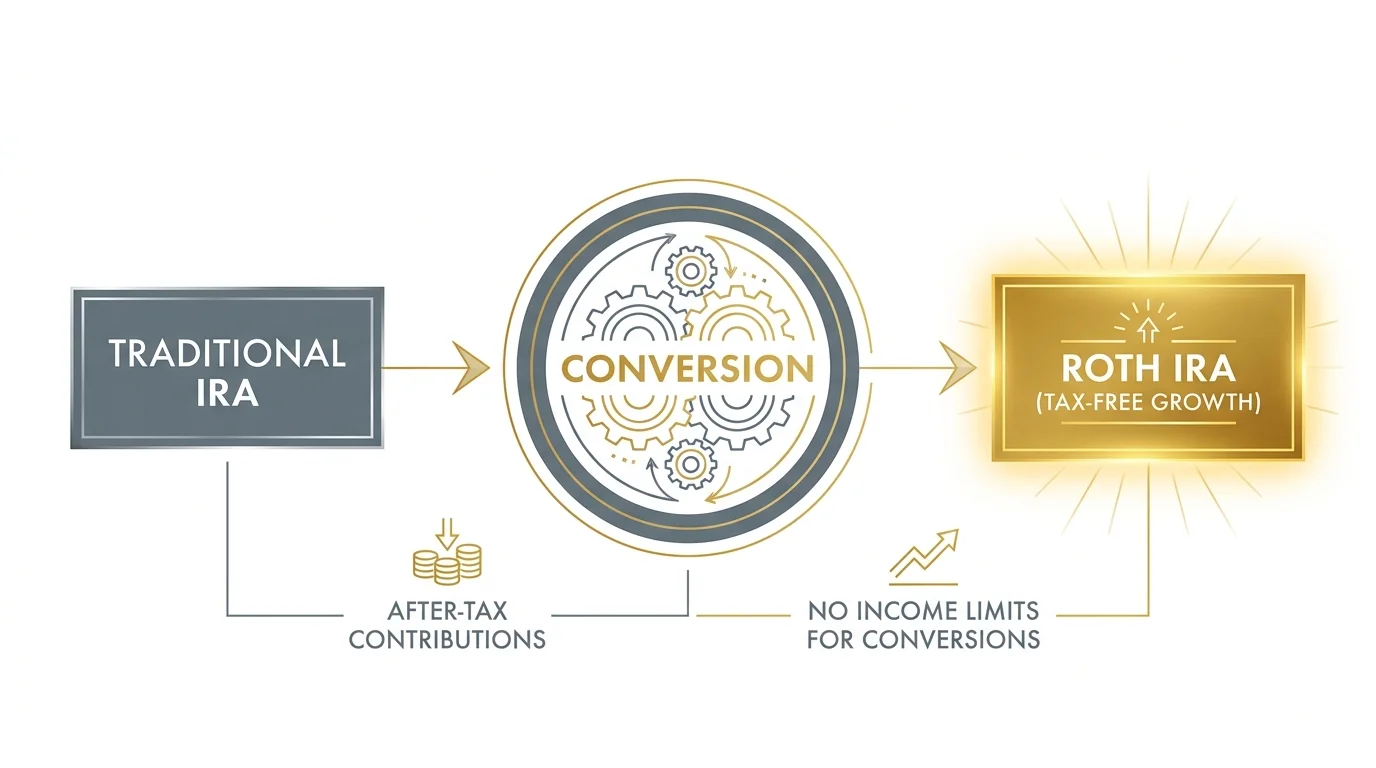

6. The Backdoor Roth IRA

A Roth IRA allows your investments to grow tax-free, and you can withdraw the money in retirement without paying income taxes. Because this is such an incredible benefit, the government places strict income limits on who can directly contribute to a Roth IRA. Once your household income surpasses a certain threshold, the IRS forbids direct contributions.

High-income earners bypass this restriction legally using a multi-step process known as a “Backdoor Roth.” First, you contribute funds to a Traditional IRA, which does not have income limits for non-deductible contributions. Next, you immediately convert that Traditional IRA into a Roth IRA. You pay taxes on any gains that occurred between the contribution and the conversion—which is usually zero if executed immediately—and the money then grows tax-free forever in the Roth account.

The IRS fully acknowledges this strategy. It allows professionals like doctors, lawyers, and successful business owners to secure tax-free retirement income that they otherwise would not qualify to receive.

7. Irrevocable Trusts for Medicaid Planning

As Americans live longer, the cost of long-term nursing care has become a primary threat to generational wealth. Medicaid pays for nursing home care, but only for individuals who have exhausted nearly all of their personal assets. Many families fear they must sell the family home and drain their savings to pay for care before Medicaid kicks in.

Middle-class families frequently use Medicaid Asset Protection Trusts (a specific type of irrevocable trust) to solve this problem legally. When you transfer ownership of your home and savings into this type of trust, you surrender direct control of the assets. In the eyes of the law, you no longer own them; the trust does.

Because you do not own the assets, Medicaid cannot count them when determining your eligibility for long-term care assistance. You can qualify for government-funded care while the trust preserves the family home and cash for your children. However, the government enforces a strict five-year “look-back” period. You must transfer the assets into the trust at least five years before you apply for Medicaid; otherwise, you will face severe penalty periods before benefits begin.