Losing a parent is an overwhelming emotional experience, and the sudden rush of legal and financial obligations that follows only compounds the grief. Navigating family finances, inheritance laws, and estate planning directives requires a clear head just when you are least equipped to make major decisions. Unfortunately, one wrong move can trigger severe financial consequences, ignite family disputes, or leave you personally liable for unresolved debts. Understanding the most frequent missteps gives you a roadmap to protect your parent’s legacy and your own financial well-being. By learning the rules before you act, you can secure the estate, communicate effectively with creditors, and smoothly handle the legal transition without adding unnecessary stress to your mourning process.

Key Concepts and Terminology Explained

Before you take any action regarding your parent’s belongings or financial accounts, you must understand the basic legal terminology. The legal system uses highly specific language to dictate who has the authority to act and how property must be transferred. Without a firm grasp of these concepts, you risk accidentally breaking the rules and delaying the entire inheritance process.

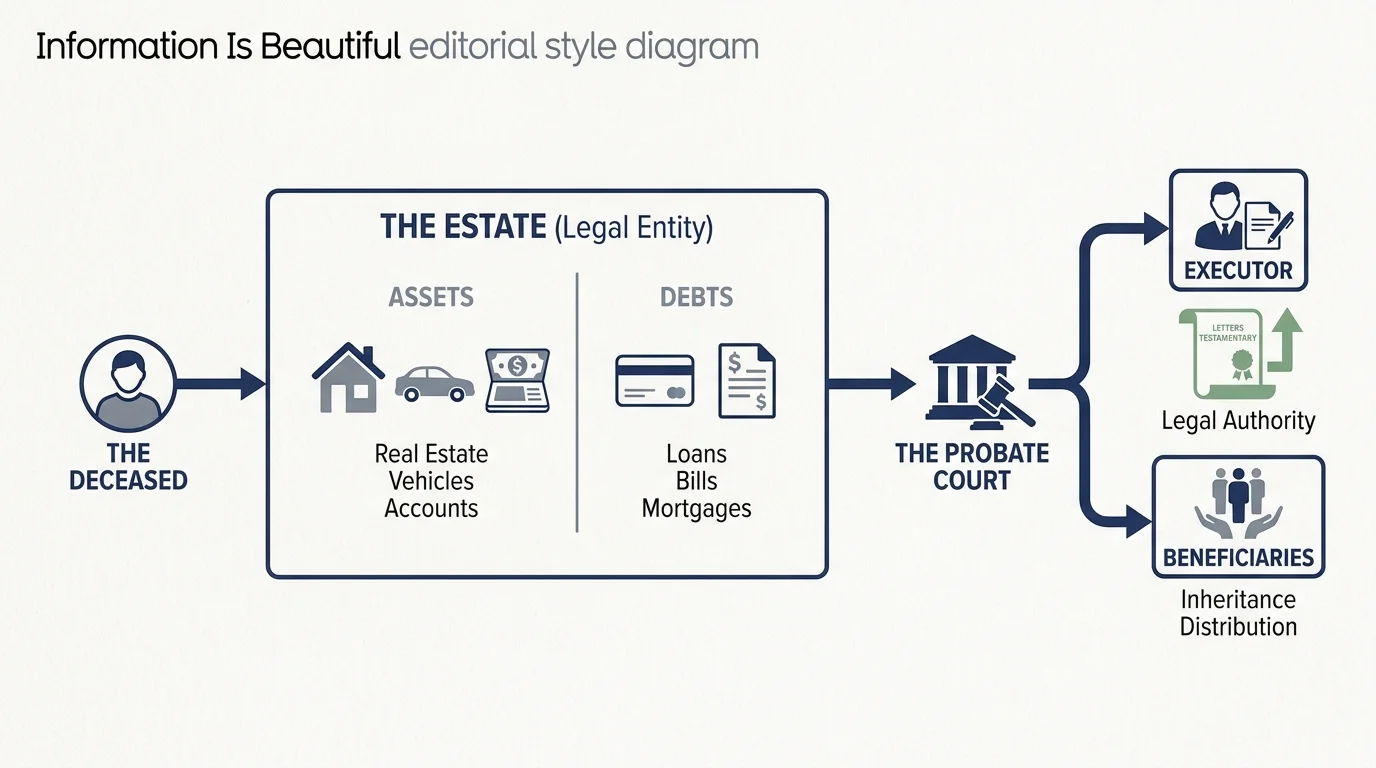

The Estate

When your parent passes away, everything they owned—their house, bank accounts, furniture, vehicles, and even their outstanding debts—automatically becomes a single legal entity known as their “estate.” You cannot view their property as your own simply because you are their child. The estate is a distinct entity that must be managed, taxed, and eventually closed according to state law before any wealth transfers to the next generation.

Probate

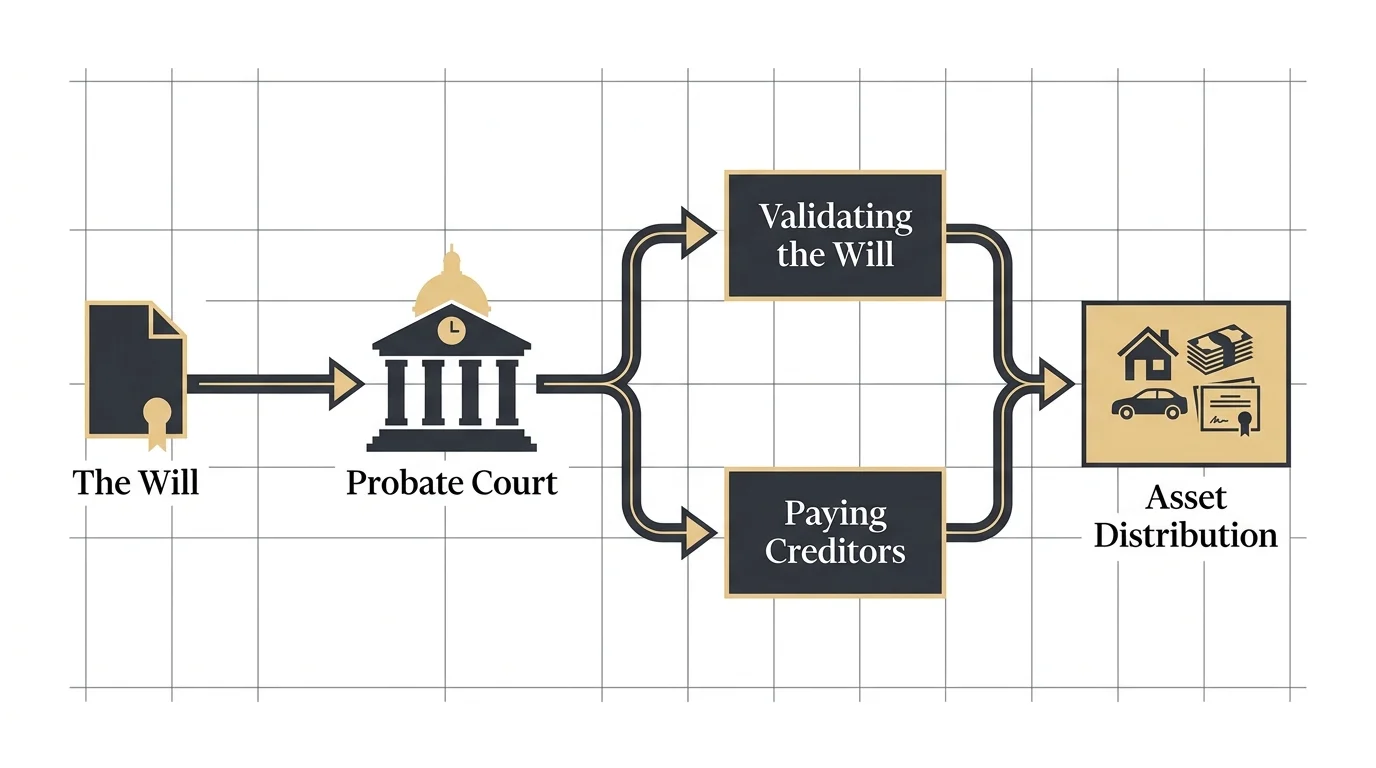

Probate is the formal, court-supervised legal process of validating a will, paying off the deceased person’s debts, and distributing the remaining assets to the rightful heirs. Many families assume that simply having a will means they avoid probate; this is entirely incorrect. A will is essentially a set of instructions to the probate court. While some assets bypass probate—such as life insurance policies with designated beneficiaries—the legal system requires a judge to oversee the transfer of most traditional property.

Executor and Personal Representative

An executor is the individual named in the will to manage the estate through the probate process. If your parent died without a will, the court appoints a personal representative or administrator to perform the exact same job. Until the court officially issues a legal document known as “Letters Testamentary” or “Letters of Administration,” the executor has absolutely no legal authority to touch the money, pay bills, or sell the house. Simply being named in the document does not grant you immediate power to act.

Intestate

If your parent died without leaving a valid will, they died “intestate.” In this scenario, state law steps in to decide who inherits the assets. Each state maintains a strict legal formula, typically prioritizing the surviving spouse and biological or legally adopted children. Dying intestate can severely complicate family finances, as the court must spend additional time identifying and verifying rightful heirs before distributing anything.

Fiduciary Duty

When the court appoints you as an executor, you become a fiduciary. This legal term signifies that you are bound to the highest standard of care under the law. You are legally obligated to act in the best financial interest of the estate and its beneficiaries, placing their interests above your own personal gain. A breach of fiduciary duty—whether intentional or born of simple negligence—can result in your removal from the position and leave you personally liable for the financial losses of the estate.