A Practical Guide to Estate Settlement

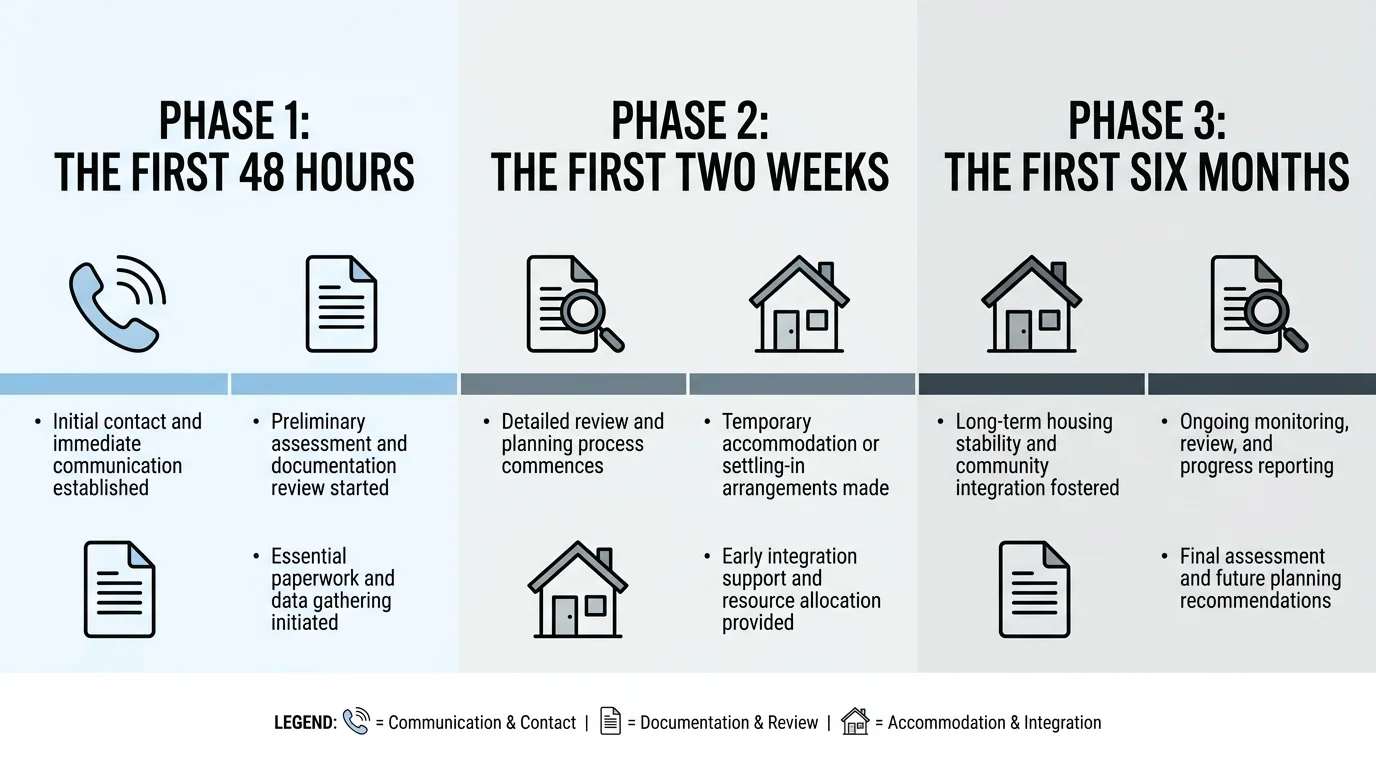

Settling an estate is not a single event; it is a prolonged administrative project that generally unfolds over many months. Approaching this process in manageable phases prevents you from feeling overwhelmed and ensures you do not inadvertently skip critical legal steps.

Phase 1: The First 48 Hours

Your immediate focus should remain entirely on your family, the funeral arrangements, and basic physical security. The law does not expect you to settle complex financial matters on the day your parent passes away. Your primary legal obligation at this early stage is to secure any unoccupied property. Lock all doors and windows, ensure vehicles are safely parked, and remove any highly portable valuables—like cash, firearms, or unsecured jewelry—to a secure, neutral location. If your parent had pets, arrange for their immediate temporary care. Do not begin dividing property, gifting mementos, or throwing things away. Simply secure the environment to prevent theft or accidental loss while you tend to the emotional needs of your family.

Phase 2: The First Two Weeks

Once the funeral concludes, your administrative responsibilities officially begin. Your priority is to locate your parent’s original will and any other critical estate planning documents, such as a living trust. These documents are typically found in home fire safes, bank safe deposit boxes, or filed away in a home office desk. Concurrently, you need to order original death certificates from the funeral director. You must also ensure that the Social Security Administration is formally notified of the death. While the funeral director often handles this initial electronic notification on your behalf, you must follow up to verify that monthly benefit payments stop immediately; otherwise, you will face an overpayment situation that the federal government will aggressively claw back.

Phase 3: The First Six Months

With the original documents in hand, you must file a petition with the local probate court to officially open the estate. Once the judge grants you the authority to act, the heavy lifting begins. You will spend the next several months taking a meticulous inventory of everything your parent owned, capturing exact values down to the penny. You must set up a dedicated estate checking account, transfer liquid funds into it, and begin evaluating incoming creditor claims. During this phase, you will also manage the physical assets, which frequently involves cleaning out the family home, conducting repairs, and preparing the real estate for public sale. Patience is mandatory during this window, as state laws require you to give creditors ample time to submit their claims before you can finalize the accounting and distribute the inheritance.